The Bear Case for S&P Global (SPGI)

CapIQ vs DIY Build with AI

S&P Global has long been viewed, me included, as one of the most durable businesses in financial services. It acts like a tollbooth on the global capital markets with irreplaceable data assets, entrenched customer relationships, and high regulatory barriers.

But the release of Claude Opus 4.6 has triggered a dramatic reassessment of that thesis.

The stock has sold off sharply alongside other software and data providers because the concern is AI will turn S&P Global’s premium data service into a commodity.

The Disintermediation Threat

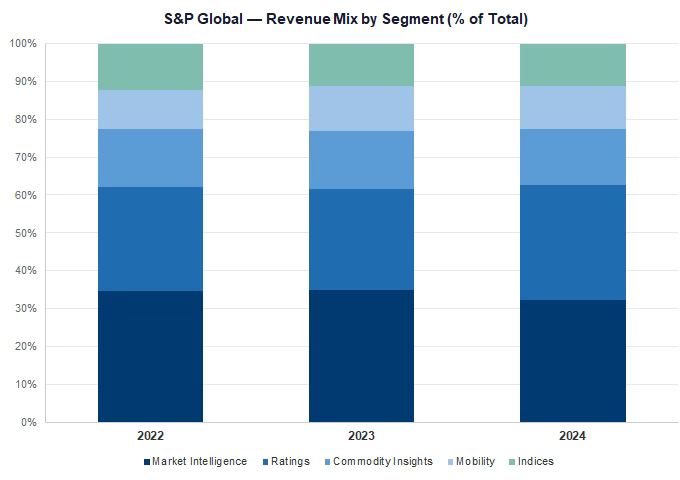

S&P Global’s Market Intelligence division—which includes Capital IQ and accounts for about 32% of total revenue—has historically commanded premium pricing because it solves a large problem for its customers: aggregating, cleaning, standardizing, and packaging financial data from thousands of different sources.

But AI models like Claude are increasingly capable of performing these exact tasks at a fraction of the cost.

Large language models can scrape SEC filings, parse earnings call transcripts, extract data from government databases, and structure it all into query-able formats automatically. The value-add that justified $20,000+ annual seat licenses is being compressed into API calls that cost fractions less.

If buy-side and sell-side firms can build internal AI systems that replicate 60-70% of Capital IQ’s functionality, the willingness to pay premium prices evaporates. Even if firms don’t cancel their subscriptions entirely, they’ll negotiate much harder on renewals, compressing both pricing power and revenue per user.

Then there’s he next generation of AI-native hedge funds, venture firms, and asset managers that may never buy Capital IQ at all.

They’ll build AI-first data stacks from day one, treating financial data as a feature of their broader AI infrastructure rather than a standalone premium product. This shrinks the addressable market over time and pressures growth.

Economics of AI DIY

Even if AI makes it easier to create your own internal system, there are still costs to build and maintain it.

Is it cheaper to outsource that headache to a dedicated financial data provider, or should you hire your own team and manage the infrastructure yourself?

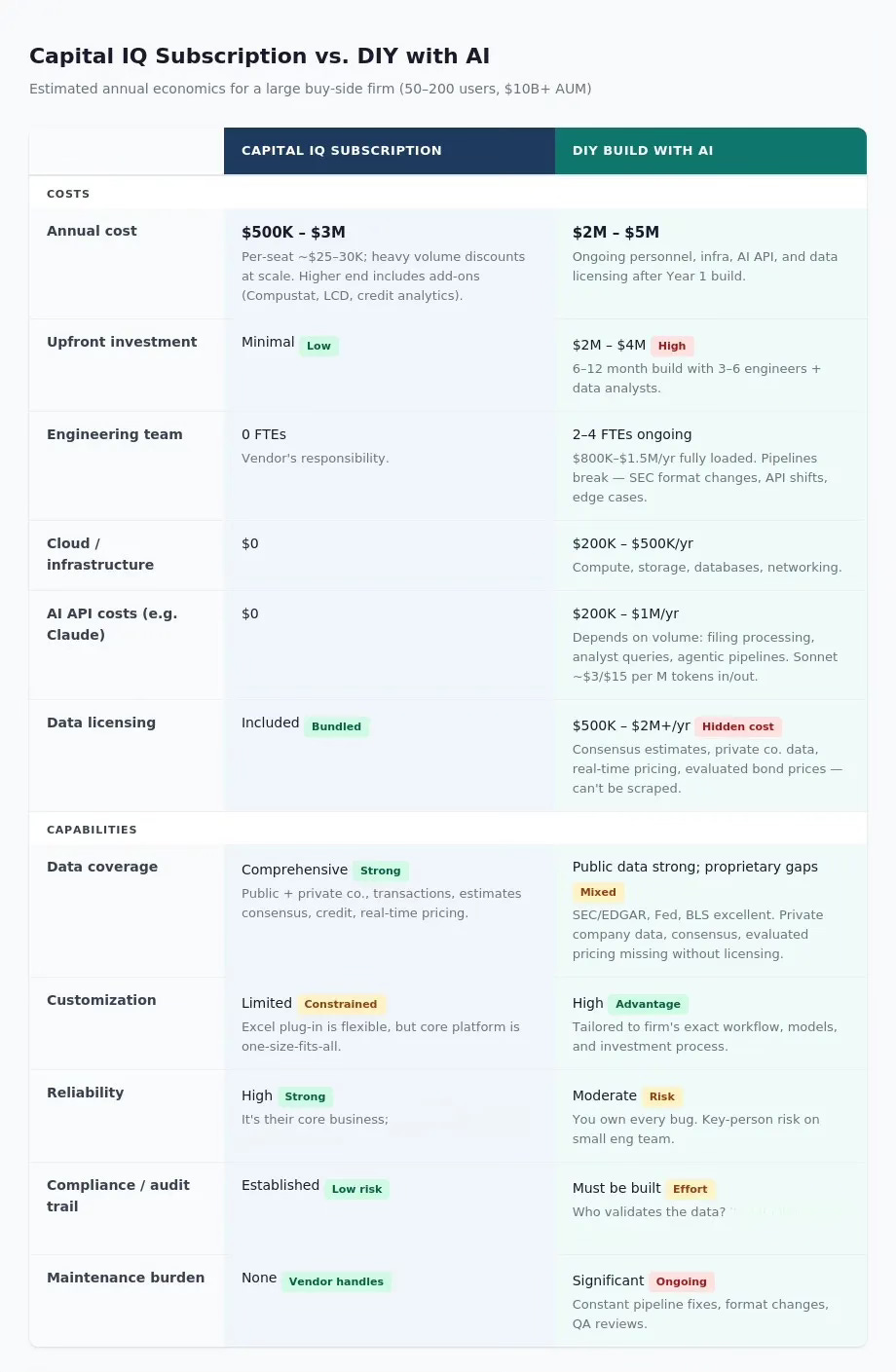

I created a table comparing the costs of building your own internal AI system versus a Capital IQ subscription for a large asset manager with around $10 billion in AUM. You can nitpick the numbers and assumptions—these were done with loose searches and, ironically, Claude queries—but I’m trying to get in the ballpark to see if it makes financial and operational sense.

I’m likely underestimating the annual costs for a Capital IQ subscription, the upfront costs to build your own system, and the ongoing maintenance costs to keep it running. But then again, maybe the ongoing maintenance costs will come down as AI assistance gets better. Again, it’s a rough comparison.

For even very large asset managers, the upfront build and ongoing maintenance costs exceed what they would pay for Capital IQ subscriptions.

The deciding factor right now is operational. It depends on how you want to work with the data.

For traditional fundamental investors, it’s too much of an operational headache. A fundamental investor’s edge doesn’t come from data engineering—it comes from security selection, behavioral discipline, and risk management.

And I’m not even accounting for the operational switching costs. Your investment teams would have to change workflows and learn a completely new system. That takes time and costs money.

But if you’re not a fundamental shop and need the customization of your own internal data system, it might make sense to replace a service like Capital IQ. However, quantitative shops are already building and relying on these internal systems because data engineering is their edge.

The hidden but significant advantage of S&P Global/Capital IQ for fundamental asset managers is the amortization of fixed data engineering costs across thousands of clients.

The Future Risk

The disruption risk right now is not mid-to-large asset managers ditching their established workflows and preferred data provider. There is too much institutional inertia and operational switching costs to justify ripping out their current workflows. And they’ll lose access to any proprietary data they get with their subscriptions.

Opus 4.6 in excel is a boon to small fundamental asset managers. You gain a junior analyst/excel monkey for fractions of what you would need to pay them in salary.

It is these firms that really only need clean public financial data that may delay the addition of an expensive data feed subscription until they absolutely need it. Or because they started with an AI first data model, they never need to add one.

A one- or two-seat subscription firm is not the most lucrative contract for S&P Global and CapIQ. But some of these firms will become large asset managers. If CapIQ is built into their workflows from the beginning, it becomes an integral piece of their operations. The firm will eventually need more seats and increased access to proprietary data turning into a very lucrative contract.

But if they build on AI first, they never add CapIQ. If enough of these firms exist, S&P Global’s Market Intelligence future revenue, profits, and cash flow are meaningfully impacted and it does not deserve a premium multiple.

The Opportunity?

The bear case is very compelling. And the rapidly shifting world of AI and technology gives it more weight.

But this is assuming that S&P Global doesn’t adjust to the new AI world and layer AI agents on top of its data subscriptions, improve its UI, increasing the value proposition of its CapIQ subscription. Or they don’t recognize the true value of their proprietary data and underprice their data feeds and API access as the demand for more data increases.

The market’s sell-first, ask-questions-later reaction is creating an opportunity to pick up data service companies with proprietary data, high customer switching costs, and network effects at great prices—like S&P Global (SPGI).

If you’re looking to add SPGI but don’t want to catch a falling knife, you can use momentum to help.

You don’t have to wait until S&P Global has positive momentum again—because you might miss out on the bargain prices. Instead, wait until the negative momentum subsides to avoid initiating a position only to watch it drop further on more negative sentiment. Yes, you’ll miss the bottom, but it helps you avoid having to make a tougher decision if the stock falls further.