Why Fair Isaac (FICO) is Valley Forge Capital's Largest Position

Using Valley Forge's own words to understand why they own so much Fair Isaac.

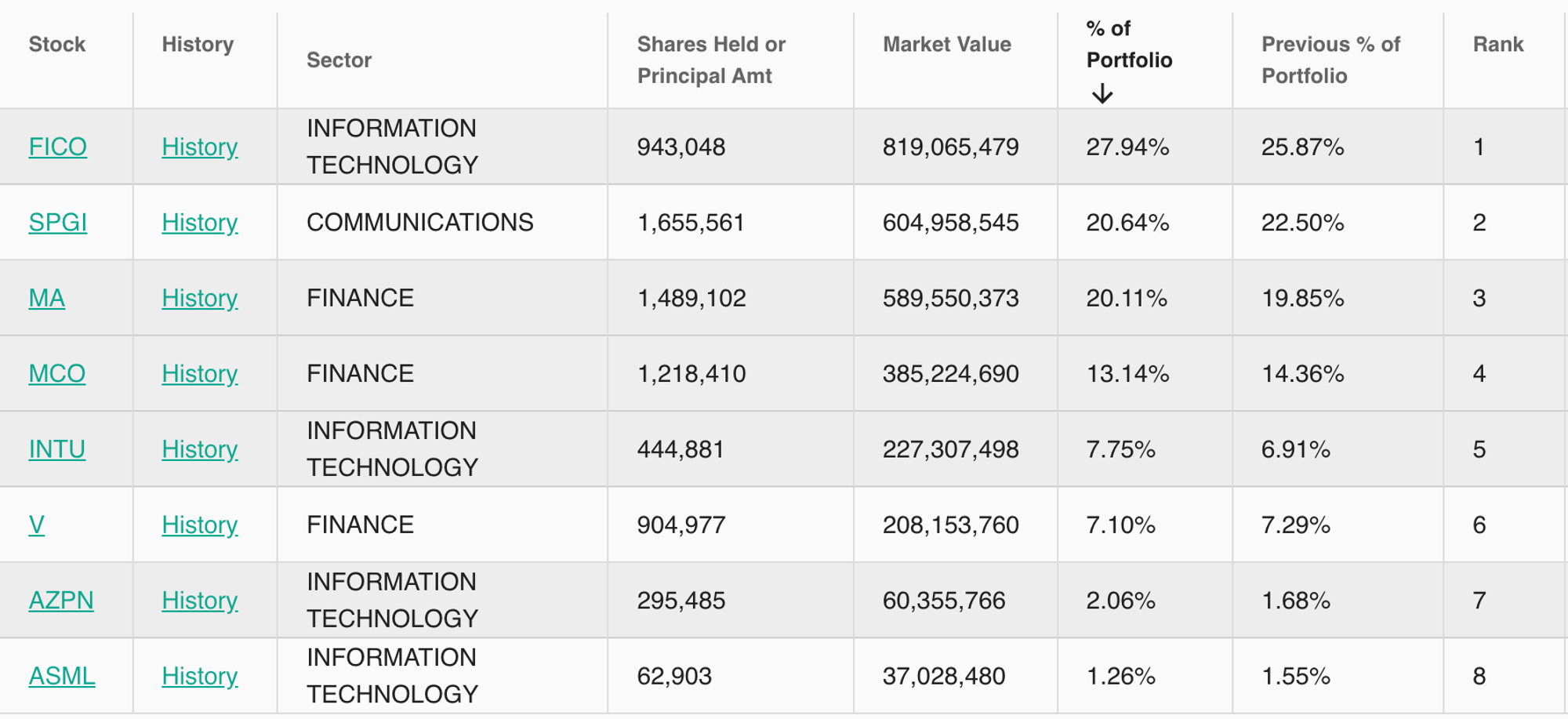

Valley Forge Capital Management runs a highly concentrated portfolio. Their latest 13-F showed 8 holdings with Fair Isaac (FICO) as their largest position at 27.94% of their portfolio.

Dev Kentesaria is a managing partner at Valley Forge Capital and I’ll use publicly available information on his investment philosophy to understand why Valley Forge owns so much Fair Isaac.

Valley Forge’s guiding philosophy is this.

We are looking for companies that provide essential products and services. That has a long history of pricing power. That has a dominant market position that we think is not subject to significant disruption. We like to see a company operate in an industry whose volumes are going up significantly over time. (18:54)

The Investor’s Podcast Episode #389

Fair Isaac’s Dominant Market Position

So some of the characteristics that we look for, we’re focused on companies that are monopolies or oligopolies in their respective industries. (19:10)

Good Investing Talks

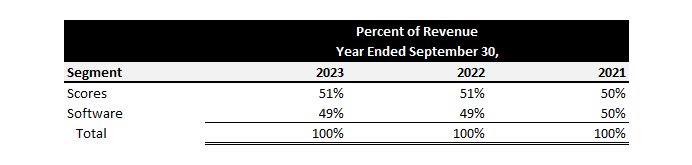

Fair Isaac has two main business divisions, scoring and software.

Scoring is the FICO score and it's essentially a licensing royalty business.

Fair Isaac does not own the data that goes into your credit score. It owns the algorithm that analyses the data to create the score. Fair Isaac licenses its scoring system to the three big credit bureaus: Transunion, Equifax, & Experian. Who then sell their data and the FICO score generated from it to lenders.

Fair Isaac earns $0.10-0.15 per score for credit cards, $0.30-0.40 per score in auto loans, and $2-8 per score for home loans.

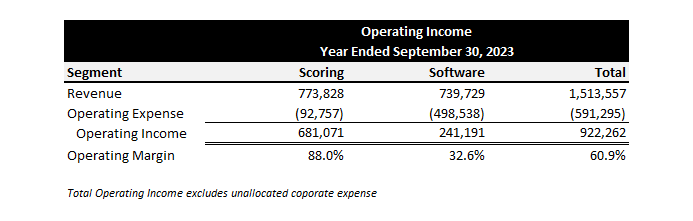

Scoring accounts for 51% of Fair Isaac’s revenue.

But with 88% EBIT Margins it accounts for about 74% of Fair Isaac’s total operating income (excluding unallocated corporate expense).

Fair Isaac has a monopoly on the U.S. scoring system. The 3 credit bureaus went so far as to create their own scoring system in 2006, VantageScore, but have been unable to dent Fair Isaac’s 90+% market share. The main reason is the FICO score is the industry standard and it is a critical piece in every consumer lending system.

Industry Standard

If you originate a mortgage and then expect to sell it to Fannie Mae or Freddie Mac to be securitized, then it must have a FICO score.

In the mortgage space, Fannie and Freddie, if you want to securitize your mortgage, sell it to Fannie and Freddie, they demand a FICO score. They want to know what's the risk on the paper. - William Lansing, CEO

And the FICO score is plugged into so many mission-critical programs to assess lending risks, that it's tough to remove. The entire risk scoring system for a lender would need to be rebuilt without the FICO score. Then the decision-making systems would need to be retrained on the new replacement score. Finally, the accuracy of the new scoring system needs to be tested and assessed. This takes time and any error in the process can detrimentally affect a lender’s viability as a going concern.

The FICO score itself is such a small cost in the entire lending decision process and a trusted measure of lending risk, that it is far easier to keep it in than to replace it. This is the exact investment Valley Forge wants.

Usually, it’s obvious that a product or service that they’re supplying doesn’t have competitors, and therefore if we like services that are cheap and essential. And so, even if prices go up 10% when inflation is 2%. We want a product or service that is a must-have for the end customer and although they may gripe about it and complain about it they ultimately will end up continue using the product because it is so important to them. [emphasis added] (42:49)

Good Investing Talks

Pricing Power

I would say pricing power is really a strong focus for us and all of the parameters that feed into organic growth. We need to see a very strong top-line and bottom-line organic growth profile and so we spend a lot of time assessing pricing power and what this looks like in the past and how that might develop in the future. (41:15)

Good Investing Talks

Lending applications are pro-cyclical. Volumes rise when the economy is booming and/or rates are declining. Then volume declines as the economy slows and/or as rates rise. Full cycle growth is going to be in line with the general economy.

Fair Isaac can grow slightly faster because they have pricing power.

Well, a ton, a ton. So the value gap is huge. We price our scores from basis points to single-digit dollars. And typically, they're used in a decision that's worth hundreds or thousands or tens of thousands or hundreds of thousands of dollars. And so the – and the score is probably the single best predictor of propensity to repay debt that there is. And so you'll obviously build other things around it, you'll check income, you'll do other things. But if you had to rely on one thing, it would be the FICO score. - William Lansing, CEO at 2023 Morgan Stanley TMT Conference

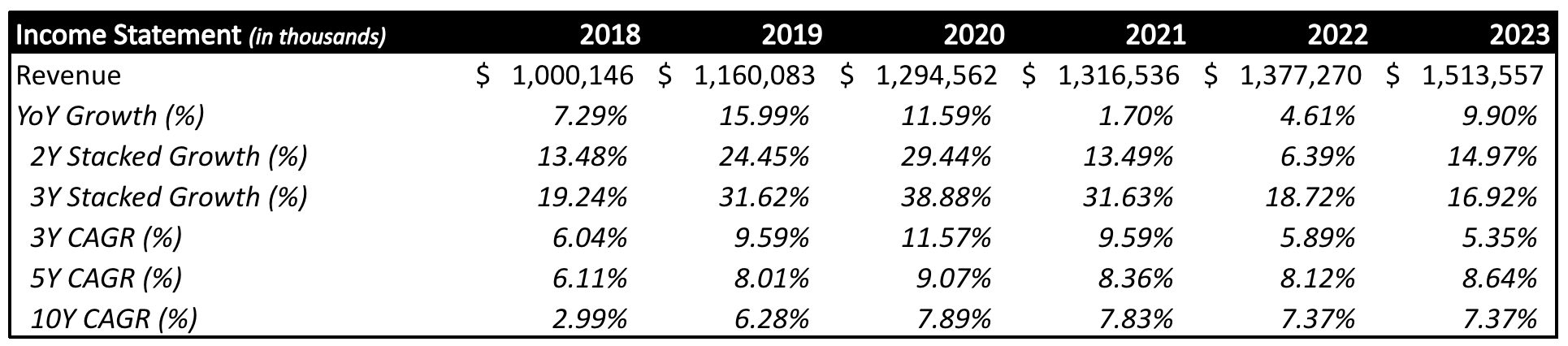

Valley Forge’s first purchase of Fair Isaac corresponds with a change in its pricing strategy. Starting in 2018, Fair Isaac raised the prices on mortgage and auto originations just in time for the recent housing and credit boom. Which fueled Fair Isaac’s recent revenue growth.

Even though Fair Isaac is essentially a monopoly on scoring, it can’t raise prices too high or too fast because then the credit bureaus and lenders are incentivized to invest in an alternative system. You want to keep raising prices just below your customer’s pain tolerance and avoid drawing the attention of regulators.

In the long run, Scoring growth should trend towards GDP plus small price increases.

ROTA, ROIC, & ROIIC

We have a high return on the tangible asset which is a good measure of efficiency for a company. We have companies that are very low in capital expenditures. (6:54)

The Investor’s Podcast Episode #389

I measure tangible assets as Total Assets less Goodwill. For returns on tangible assets (ROTA), I take the Current Net Income and divide it by the average Tangible Assets from this year and the previous year.

I prefer to look at returns on invested capital (ROIC) and returns on incremental invested capital (ROIIC).

Given its strong competitive advantages and the minimal amount of CAPEX needed to maintain and grow its scoring business, Fair Isaac also generates high returns on invested capital.

Returns on incremental invested capital (ROIIC) let us know if the company still has high returning reinvestment opportunities. Based on the 1-year , 3-year, and 5-year ROIIC Fair Isaac still has high reinvestment opportunities.

The negative ROIIC in 2022 only happens because there’s a decline in invested capital not a decline in NOPAT. This is a testament to how little capital is needed to maintain and grow the business.

Free Cash Flow Machine

we also want to find the companies that have the most promising gap between the free cash flow yield at which they’re trading today and what free cash flow yield we think they should be trading at. So for example, Moody’s. There have been times when Moody’s has traded at a 5% or 6% free cash flow yield. If you go back 10 or 12 years they might have even traded at a 10% free cash flow yield and we may have determined based on business quality that in fact they really should have been trading at a 3% free cash flow yield relative to the risk-free rate. (47:28)

The Investor’s Podcast Episode #389

Over the last 10 years, Fair Isaac grew its FCF per share at a compound annual growth rate of 17.2% and it accelerated over the last 5 years to 21.6%.

Because of Fair Isaac’s low fixed-cost structure, especially in its scoring business, it converts a large percentage of its revenue into free cash flow.

But has Fair Isaac traded at a mismatch between its trading FCF yield and its potential?

It’s traded at FCF yield well below its median yield since Valley Forge first bought Fair Isaac.

But over the last twelve months, Fair Isaac generated $495.3 million in free cash flow and Fair Isaac’s market cap at the end of June 2018 was around $5.7 billion. The FCF yield on their cost is close to 8.7%.

A 3% FCF yield was a decent price to pay for free cash flow that would go on to compound over 20% for the next 5-6 years and it’s a great price if Fair Isaac can continue to compound its FCF at 20+% over the next 5 years or longer.

Capital Returns

Management should also have a strong and consistent record of using the free cash flow the company generates in a prudent manner, whether buying back stock, paying dividends or reinvesting in the business.

Value Investor Insight

Given its high returns on invested capital, Fair Isaac needs to reinvest a minimal amount of capital back into its business to reach its target growth rates. This leaves a lot of excess capital it can return to shareholders, and it does so in the form of share buybacks.

Over the last 10 years, Fair Isaac has bought back 27.9% of its shares outstanding.

According to Whale Wisdom, Valley Forge first bought Fair Isaac in Q2 2018. Since June 30, 2018, the end of Q2 2018, Fair Isaac returned 564% or 40.4% compounded annually as of January 26, 2024.