The SaaS Hierarchy: Why Some Software Is Irreplaceable (And Some Isn't)

A framework for categorizing SaaS companies by defensibility & survivability

Claude’s recent code launch is often cited as the sole reason for the dramatic sell-off over the last few days, but it was more the catalyst—the point of nucleation that crystallized many recent SaaS fears.

Long Duration Asset

SaaS is a long-duration asset. Most of its profits and value are expected years from now, when the company has built a significant customer base and operating leverage kicks in to boost profit margins and cash flow.

Long-duration assets are very sensitive to interest rates. After some initial cuts, the Fed Funds rate has not come down, and the U.S. 10-year rate has actually increased. If rates remain higher for longer, the price of long-duration assets must come down.

Slowing Growth

Each SaaS company is different, but the sector as a whole is seeing slower seat expansion. Companies are scrutinizing their software budgets harder, focusing on which software is a need-to-have versus a nice-to-have.

The rule of 40 has been used to help value SaaS companies. If revenue growth is slowing, they don’t deserve a high P/E ratio.

Slower revenue growth means operating leverage kicks in even later, pushing future cash flows further out and requiring a lower market multiple today.

IT Budgets

The current shifting business and geopolitical environment is moving IT budgets from a growth phase to a cost control phase.

Companies are reviewing their software spend and cutting what they don’t need to survive. This creates longer sales cycles and increased pricing pressure when renewals come up.

Again, operating leverage and future profits get pushed back, requiring a lower multiple today for SaaS companies.

Crowded Ownership

SaaS was and is a crowded market, and for good reasons. There are many high-quality companies with immense switching costs, network effects, and pricing power. But not every SaaS company has these. As the great companies rose in price, the entire industry benefited from passive flows into the sector, and SaaS names dominated many active fund portfolios.

When a risk-off moment happens, you get dramatic changes in flows. It’s the classic stairs up, elevator down movement.

Claude

Claude’s recent code launch was the nucleation point for all these fears.

Claude and Vibe coding reduce the barriers to entry for competitors. It doesn’t mean someone can spin up an exact feature-rich replica that encompasses all the features of a SaaS offering, but could they spin up a competent replica that meets their specific needs? Could it delay their need to pay for the full feature-rich software? How defensible is SaaS revenue in the era of vibe coding? How much pricing power do SaaS companies have when there’s a credible alternative?

SaaS companies, as long-duration assets, are highly susceptible to changes in net dollar retention. Increased price concessions, slower seat expansion, and longer sales cycles will cause large multiple resets lower.

The recent sell-off is that rerating. And like most reratings, it’s quick, dramatic, and indiscriminate. When indiscriminate selling occurs, we can find opportunities.

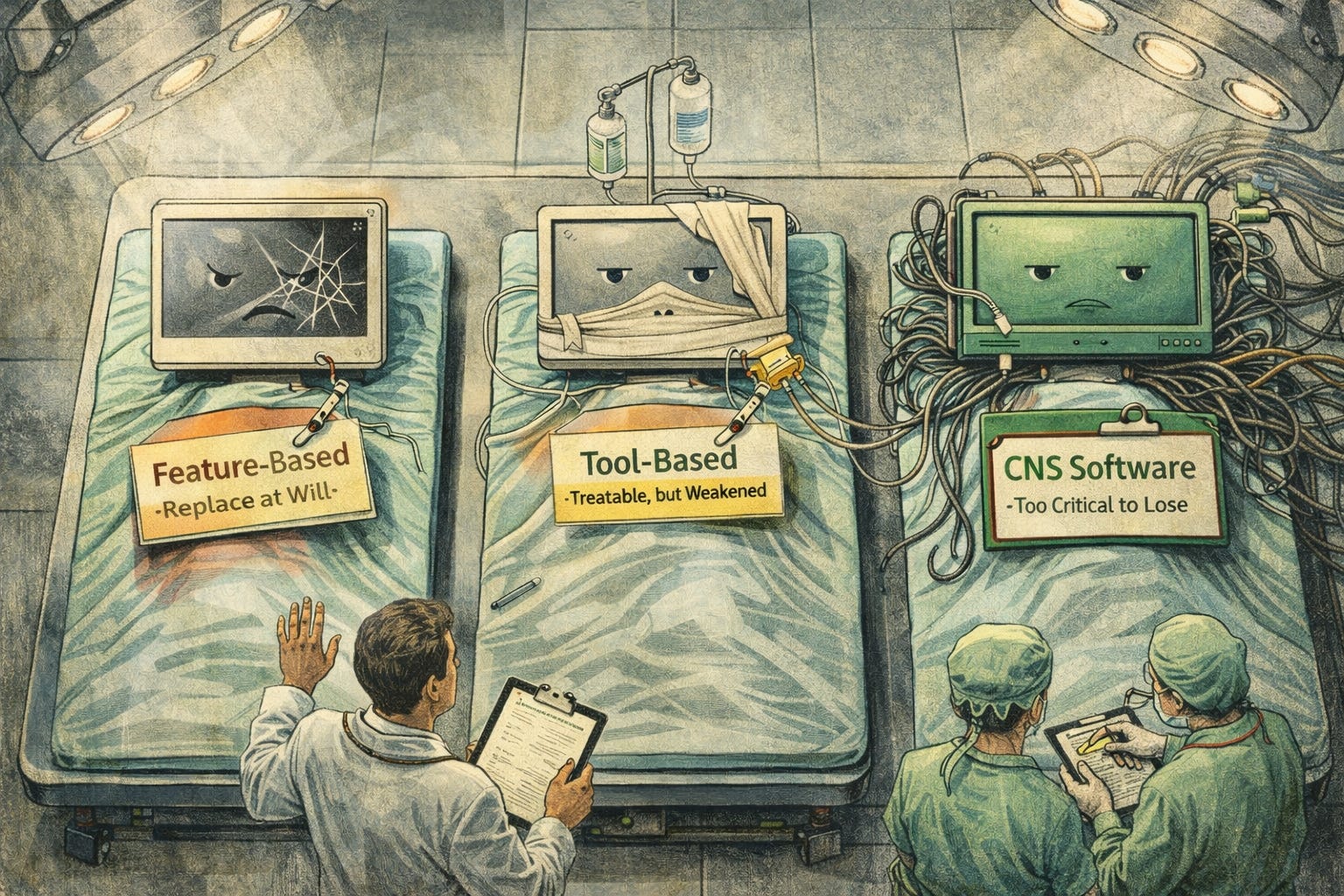

The key question to ask: if this software vanished tomorrow, what happens?

If it’s an annoyance, then that SaaS company is feature-based. Feature-based software is just a simple layer on top of another product. The goal is to improve speed or organization. Think task managers, note-taking apps, scheduling tools, or dashboard visualizers.

These simple layers and features are most at risk from vibe coding.

Do workflows slow down, and overall productivity drop off?

Then these SaaS companies are tool-based.

Tool-based SaaS companies sit inside real workflows and are part of important internal processes. They increase speed and accuracy.

It will come down to a case-by-case basis, but these are at threat too. They no longer deserve the high multiples from before because some companies can create a decent vibe-coded replica or delay their need for the full feature-rich tool set. Maybe they just need one specific tool right now and could do without the rest—and now they don’t have to pay for it.

Claude's code is not an existential threat to these companies, but it does reduce future seat count, delay price increases, and cause market multiples to shrink.

If the answer is it’ll cause a major financial issue, legal issue, or potentially a full operational stop, then these SaaS companies are least likely to be hurt by vibe coding. They’re more likely to benefit from integrating AI into their businesses and services. Adding AI services on top of their core products should increase customer switching costs and maintain their pricing power.

These are Central Nervous System Software companies. They’re too important to try to replace with a homegrown product. The customer needs 100% functionality all the time.

These companies don’t deserve the drastic rerating like the other SaaS companies. They may not regain their previous high market multiples, but they certainly don’t deserve to trade like their business is in jeopardy.

Position Updates

I’ve recommended a couple of Central Nervous System Software stocks for the portfolio, and they didn’t escape the recent market sell-off. Two financial data providers also got hit by AI fears. I’ll address them in another update. For now, I’m going to focus on the two SaaS companies.