The Rebirth of a Titan - GE Aerospace

Few names in American business history carry as much weight as General Electric. Founded by Thomas Edison in 1892, GE has long been synonymous with industrial innovation and engineering excellence. From light bulbs and home appliances to jet engines and healthcare technology, GE has touched nearly every aspect of modern life. However, the company’s journey has not been without challenges. Over the past few decades, GE faced significant hurdles, including financial crises, shifting market dynamics, and the need to streamline its sprawling operations.

Today, GE stands at the dawn of a new era, reborn as GE Aerospace. This transformation is the culmination of years of strategic restructuring, divestitures, and a renewed focus on its core strengths. GE Aerospace represents not just a rebranding but a fundamental shift in the company’s vision—an intense focus on innovation in the aerospace and defense sectors, industries poised for sustained growth in the 21st century.

As a standalone entity, GE Aerospace is now free to harness its engineering prowess and operational expertise to capitalize on the booming demand for next-generation aviation technology.

Quality Factors

High Barriers to Entry

Duopoly

The commercial jet engine business has two different end markets, wide-body jets (twin aisle) and narrow-body jets (single aisle).

Two companies dominate each end market. GE Aerospace and Rolls-Royce dominate wide-body engines. GE Aerospace and Pratt & Whitney dominate narrow-body engines.

Measured by its total engine install base of 40,000 plus commercial engines, GE Aerospace participates in about 75% of the commercial jet engine market.

It took years and massive capital investments in R&D and in manufacturing facilities by GE Aerospace to reach this position. It would be extremely cost-prohibitive for a new entrant to the jet engine market to compete for GE Aerospace’s business. Even if a potential competitor were able to raise the capital to build out their manufacturing capabilities, could they reach the same economies of scale that GE Aerospace has reached to make the effort economically worth it?

R&D

GE’s R&D spend has consistently produced stronger more fuel-efficient engines with impeccable safety ratings. It’s why GE Aerospace earned a leading position in jet engine manufacturing and it creates a self-reinforcing positive cycle.

GE’s leading manufacturing position gives it better economies of scale than its competitors leading to higher operating margins. This creates a virtuous cycle. Higher margins allow GE to reinvest more capital as a percentage of revenue back into R&D. The increased R&D allows GE to maintain its current market position and invest for future growth.

High Switching Costs

The jet engine business also comes with incredibly high switching costs

Once an aircraft is configured to a specific engine, it is extremely difficult to switch to another engine brand. It requires major changes across the whole plane like the mounting pylon, the wiring and ducting, instrumentation, and avionics systems. The aircraft would be out of commission for a long time and every minute that plane is not flying it is losing money. It’s not financially worth it to change engines.

Airlines have built out their maintenance, repair, and overhaul (MRO) services to be as efficient as possible and focused on servicing as few jet engine types as possible.

Not only would it be costly and time-consuming to switch engines on a plane, but it would also be costly to retool and reconfigure your MRO services.

If you’re a smaller jet engine maker trying to gain market share against GE Aerospace you have to wait for the next cycle of new aircraft to try and get your engines onto planes and into fleets. But then you face two more problems.

Long Operating life

Commercial jets and their engines are built to operate for 20+ years. If you're a competitor that wants to gain market share when the next airplane build cycle comes around, you’ll have to wait 20 years and continue to invest in R&D to ensure that your engine is a viable option.

Without an existing commercial engine business, it is tough to justify a 20-year cycle of investment with the hopes that your engine gains market share.

The last hurdle is GE Aerospace’s long track record of safety and your lack of one.

Safety

David Rubenstein: What is the most important issue when people buy jet engines?

Larry Culp: Safety. Safety. Safety.

A plane crash is one of the most visceral tragedies in the modern world. It’s not just the sudden massive loss of life but the fear it instills in all of us as would-be travelers.

Even if a crash were 100% out of an airline's control, they could still face a consumer backlash. Airlines already operate with thin profit margins and any consumer backlash could push the airline into the red. Airlines want the safest planes and the safest engines.

GE became the first company that designed its engines to be recognized by the FAA for its safety management systems.

And GE Aerospace has a long history of safe engine operations.

Does an airline put its entire operation at risk and switch to new jet engine maker or stay with a company with a long-proven track record of safe operations? GE’s multidecade track record of safety creates an incredibly high switching cost.

Catalysts

Narrow Body Plane Demand

New narrow-body jet engines like GE Aerospace’s LEAP are 15-20% more fuel efficient than older model engines.

Airlines are ordering new narrow-body planes with new fuel-efficient engines to replace older planes. The cost savings from operations alone justify the cost of a new plane.

The LEAP engine also provides more thrust than older models. More thrust with greater fuel efficiency allows narrow-body planes to fly further — and most importantly — profitably. This increases the connectivity between secondary and tertiary airports that might have been too far apart before. This opens up more routes for airlines to operate.

Transatlantic flights, 8+ hours, are dominated by wide-body jets but new narrow-body planes with newer engines can make the crossing. JetBlue wants to start flying to Europe from Boston and New York as they replace their older Airbus A320 & A321 planes with newer ones and newer engines.

Over the next 20 years, Boeing expects airlines to order over 42,000 new jets. Driven mostly by low-cost carriers and the narrow-body planes that they operate.

PARIS, June 18 (Reuters) - U.S. plane maker Boeing slightly raised its annual 20-year forecast for new jetliner deliveries, propelled by the strength of the narrow-body market fueled by demand from low-cost carriers.

Boeing expects airlines will need to buy 42,595 jets from now until 2042, up from 41,170 planes in its previous 20-year forecast last year.

LEAP engines are fairly new but the addition of so many narrow-body planes could drive significant growth in GE’s service revenue and service revenue has a higher margin profile.

ROIC Growth

The jet engine business model is a higher-cost higher-tech version of the razor/razorblade model.

Jet engine manufacturers sell their engines at a big discount to earn long-term service contracts to maintain the engine. These contracts usually run for 15+ years. Servicing jet engines has higher margin revenue and generates higher returns on capital.

Right now the new LEAP engine accounts for a small percentage of shop visits. But as deliveries increase and LEAPs become a larger part of fleets the servicing revenue driven by LEAP engines will grow, increasing future operating margins and future returns on capital.

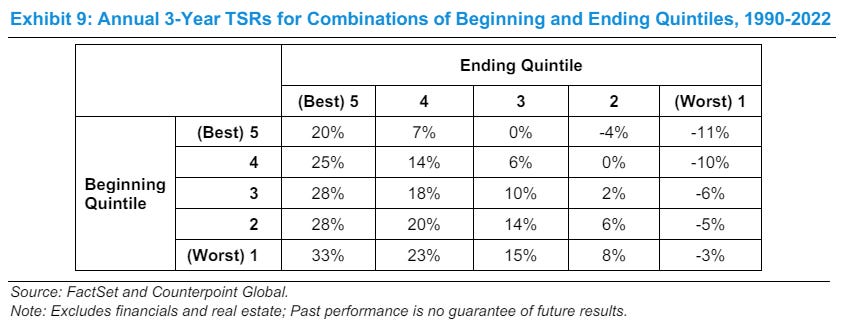

According to Michael Mauboussin and Dan Callahan, ROIC growth is a component of strong total shareholder returns.

Capital Return

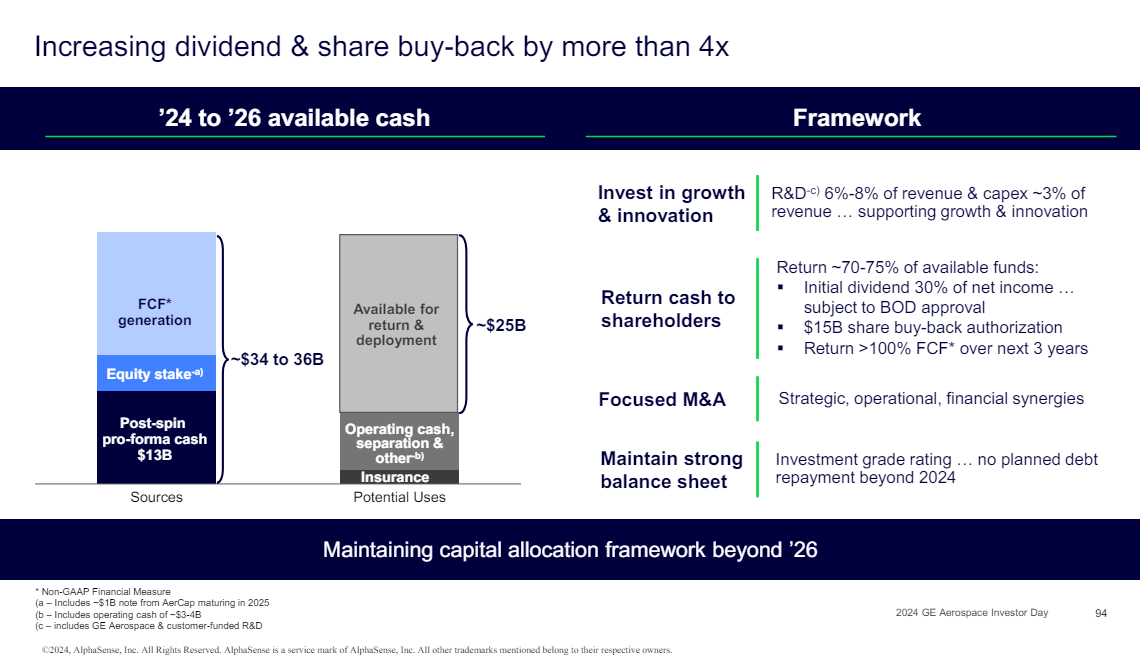

The second component of strong shareholder returns from a growing ROIC is the weighted average cost of capital (WACC). If GE can maintain a consistent WACC — some things are out of its control like the risk-free rate — while growing its ROIC then this creates excess capital and free cash flow that GE can return to shareholders through increased dividends and share buybacks.

GE Aerospace’s management wants to return a minimum of 70% of its free cash flow to shareholders through dividends and share buybacks and 100% of free cash flow over the next 3 years.

Management initiated their capital allocation plan with a 250% dividend increase after spinning off GE Vernova.

Risks

Poor Product

Long-term service contracts for jet engines are great if the engine is good. Service contracts push the cost of maintenance and the liability back to the OEM.

If the engine is poorly built this increases the cost to service and repair the engine. What was once a potentially high-profit business is now potentially a money loser.

If GE’s LEAP engine turns out to be a poor product then the high service cost to maintain them will depress future profit margins and lead to a declining ROIC. As the table above shows, the worst returning stocks are those with declining ROICs.

Travel Decline

Travel demand is rising because there is still some pent-up demand leftover from the pandemic, a growing global populace with a desire to travel, and increasing global wealth allowing more people to afford to travel.

But if travel demand were to stagnate or decline this would decrease the need for new airplanes, which reduces the need for new jet engines that GE Aerospace manufactures. Also, fewer planes in operation would mean less need for the maintenance and servicing of existing engines which is a large part of GE Aerospace’s business and future profits.

Valuation

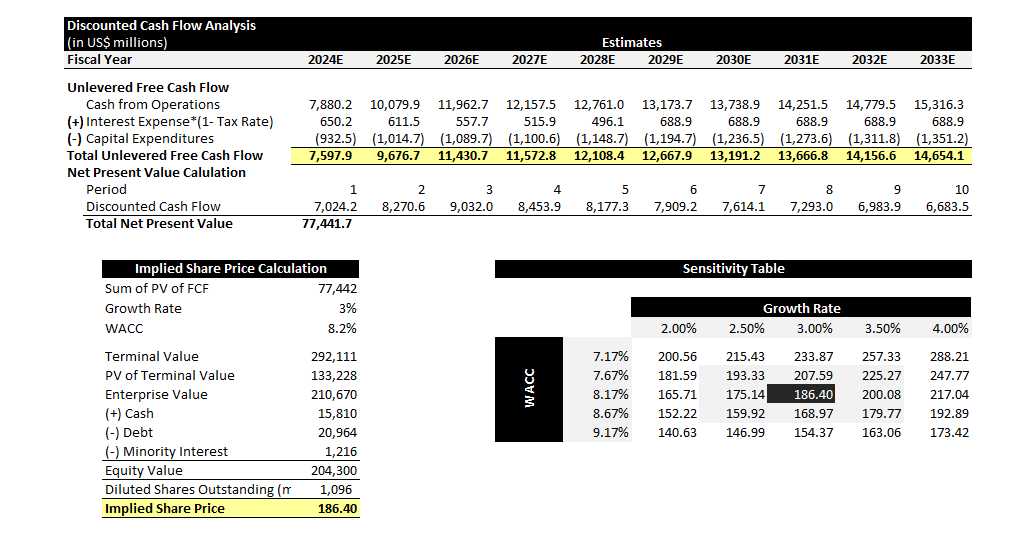

Our estimate of fair value based on a discounted cash flow model is $187 per share.

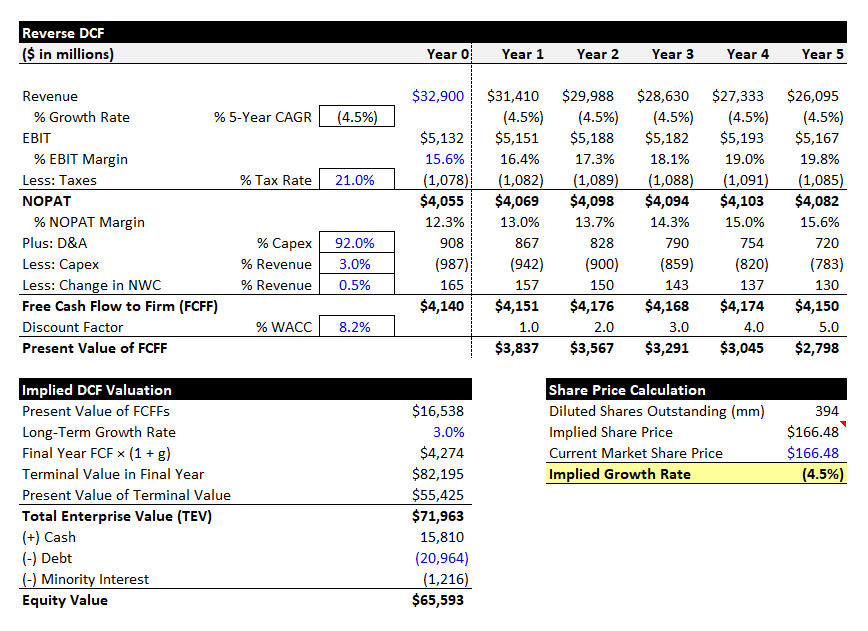

But we also want to understand what expectations the market is pricing in today by using a reverse DCF.

We expect GE Aerospace’s EBIT margins to improve from 15% to 20% as it continues to improve and streamline operations and as higher margin service revenues for its LEAP engines grow. But at today’s price, it appears the market is not pricing in margin expansion because revenue growth is not needed to justify today’s price. The reverse DCF above shows negative 5 year CAGR revenue growth is needed to justify today’s share price if EBIT margins expand from 15% to 20%.

Even though GE Aerospace may look expensive based on a P/E ratio and when comparing it to similar companies, it appears the market is not giving enough credit to GE’s potential margin expansion and growing demand for its newer more fuel-efficient jet engines.

Recommendation

Buy GE Aerospace (GE) up to $187 per share.