The Paychex (PAYX) Bear Case

AI disruption, payroll competition, a jobs index below 100, and falling float income

Back in January Anthropic shipped Claude Cowork.

Within hours, software stocks started bleeding, and by the end of the month, $170 billion in market cap had evaporated.

It was The SaaS-pocalypse.

If an agentic AI can write code, draft emails, summarize documents, and handle structured workflows at near-zero marginal cost, then the application layer is at risk. Anything that was or looked like a “SaaS” company was vulnerable until proven otherwise.

Paychex got dragged in with them.

Down around 40% from its most recent 52-week high.

But Paychex isn’t a SaaS company.

It’s a payroll processor with a PEO business stapled on that has a regulatory moat built in.

The AI-replacement story that wrecked SaaS companies doesn’t map cleanly onto a business whose customers pay it to not get audited.

But there is an AI adjacent element to the bear case and AI disruption is the loudest story in the market and the one getting the most attention even for companies like Paychex.

The Four Bear Narratives

The bear case against Paychex is composed of four narratives.

AI and Advisory Pricing

Paychex sells payroll at the core, but the margin lives in the HR consulting, compliance guidance, and PEO advisory wrapped around it. That’s where the take rate sits.

The concern is that agentic AI eats away at the HR, compliance, and PEO advisory business.

Routine HR questions like “what’s the I-9 deadline?”, “how do I classify this 1099?”, “what’s the FLSA threshold this year?” are exactly the kind of structured, rule-based queries large language models handle. You don’t need 80% of Paychex’s advisory function to get replaced. 30% of its highest-margin layer being competed away is enough to change the future value of the business.

Even though AI disruption is the most salient risk right now across the market. I don’t see it as an immediate risk to Paychex’s advisory business because of behavioral inertia and major legal barriers.

If an SMB is using Paychex and it solves all their payroll and/or compliance needs, then why switch? Yes, there are cheaper payroll companies, which I’ll talk about below, but then you’ll also need to replace your HR and compliance. It’s a hassle, and unless a small business is really at their breaking point with Paychex, they’re unlikely to get distracted by a new project that doesn’t grow their business.

For the AI disruption narrative, the biggest hurdle is liability.

Paychex’s HR and PEO business is not just selling a service; it’s selling indemnification.

Someone has to sign the 941.

Someone has to be the named defendant when an employee files an EEOC complaint.

Someone has to hold the workers’ comp master policy and carry the ERISA fiduciary duty on the 401(k).

The IRS is not going to accept “the AI told me to” as a defense. AI cannot be sued, cannot be deposed, cannot be an insurance counterparty, cannot owe fiduciary obligations to a plan participant. These are structural properties of being a legal person with assets.

With PEO or co-employment, Paychex becomes the employer of record on the W-2. The IRS certified them as one of fewer than 150 CPEOs in the country, which requires quarterly bonding, audited financials, and confers sole liability for federal employment taxes on the PEO itself.

Sure, an LLM can answer basic questions and handle basic consulting, but it can’t sign the return, post bond, hold the policy, and absorb a lawsuit.

Increased Payroll Competition

Payroll, Paychex’s original business, has been commoditized, and you can argue it is losing ground to newer software-native companies like Rippling, Gusto, and Deel. That is one reason Paychex bought Paycor: to strengthen its position at the upper end of the market. But at the low end, the new-business-formation cohort is increasingly turning to modern, tech-native payroll platforms with better UIs.

The AI disruption narrative is also at play here, with the assumption that SMBs will vibe-code their own system.

Again, this skips over the legal and liability hurdles.

Every state or local jurisdiction has its own filing frequency, deposit schedule, withholding tables, unemployment insurance rate, and rules for sick leave accruals, tip credits, and supplemental wage rates. New York City alone has roughly 40 distinct payroll-related compliance touchpoints. The IRS assesses about $13 billion annually in payroll tax penalties. Roughly 40% of small businesses get hit with at least one payroll-related penalty per year if they self-file.

Paychex’s major selling point is that it will eat the penalty if it messes up. Again, it’s selling SMBs indemnification. A vibe-coded solution opens up the SMB to increased liability.

But a cheaper software native solution that provides the same payroll efficiency and liability protection is a bigger immediate concern.

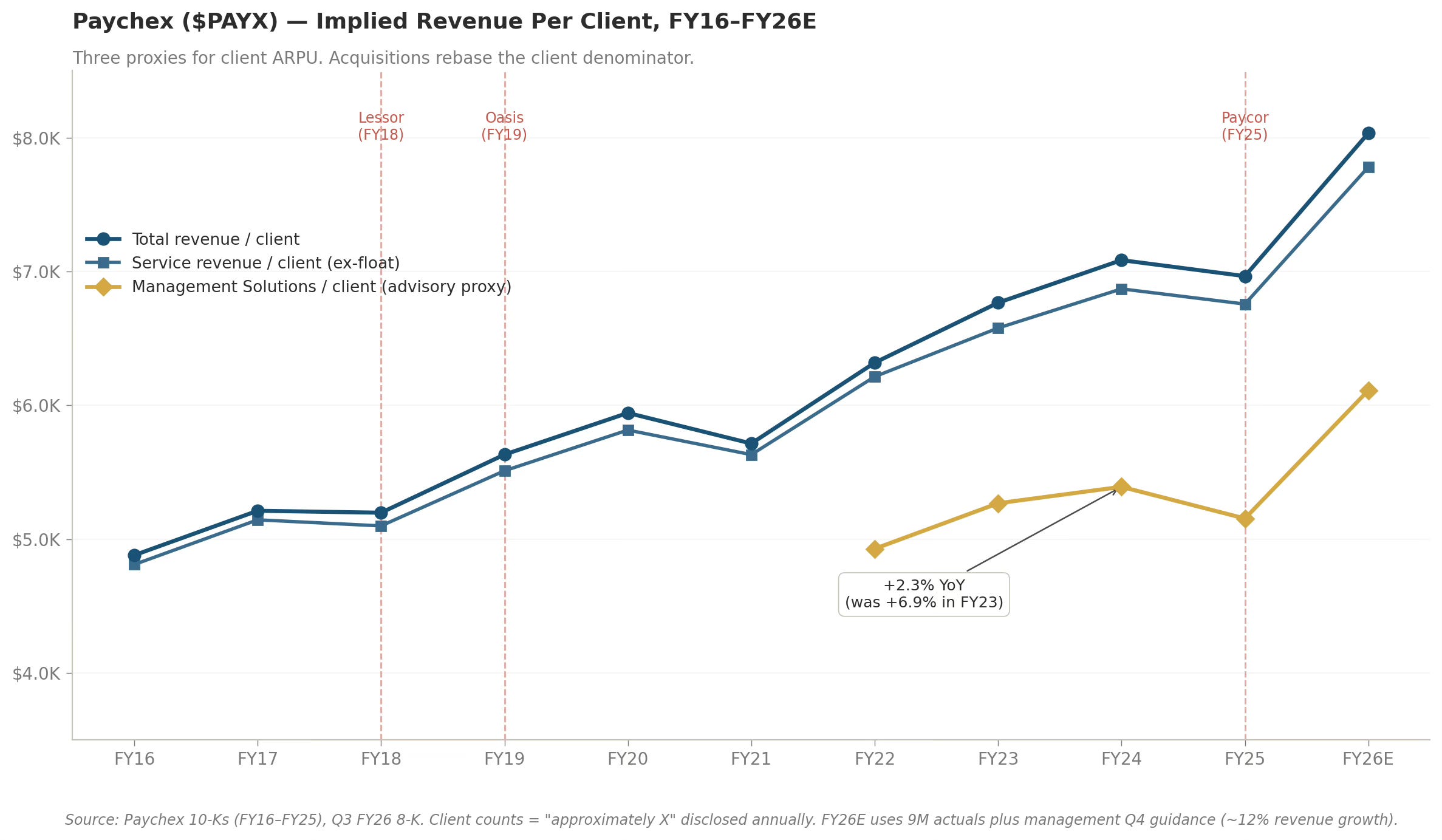

Management Solutions ARPU growth, the closest available proxy for advisory pricing per client, decelerated from +6.9% in FY23 to +2.3% in FY24, before the Paycor deal closed.

Paychex does not disclose ARPU directly, but it does disclose total revenue and approximate client count. The three proxies break PAYX’s estimated ARPU into three parts: total revenue per client (broadest, includes float), service revenue per client (ex-float), and Management Solutions per client (the closest thing to an advisory ARPU). The acquisition lines flag Lessor, Oasis, and Paycor, where the denominator gets rebased.

Paychex is not dying.

The PEO business is growing.

Payroll tax compliance across 50 states is not getting easier.

But the ARPU deceleration suggests its pricing power is fading.

PAYX’s acquisition strategy is about buying growth and moving upmarket because the organic flywheel is slowing at the lower end. It’s a defensive move to combat the encroachment of software-native competitors.

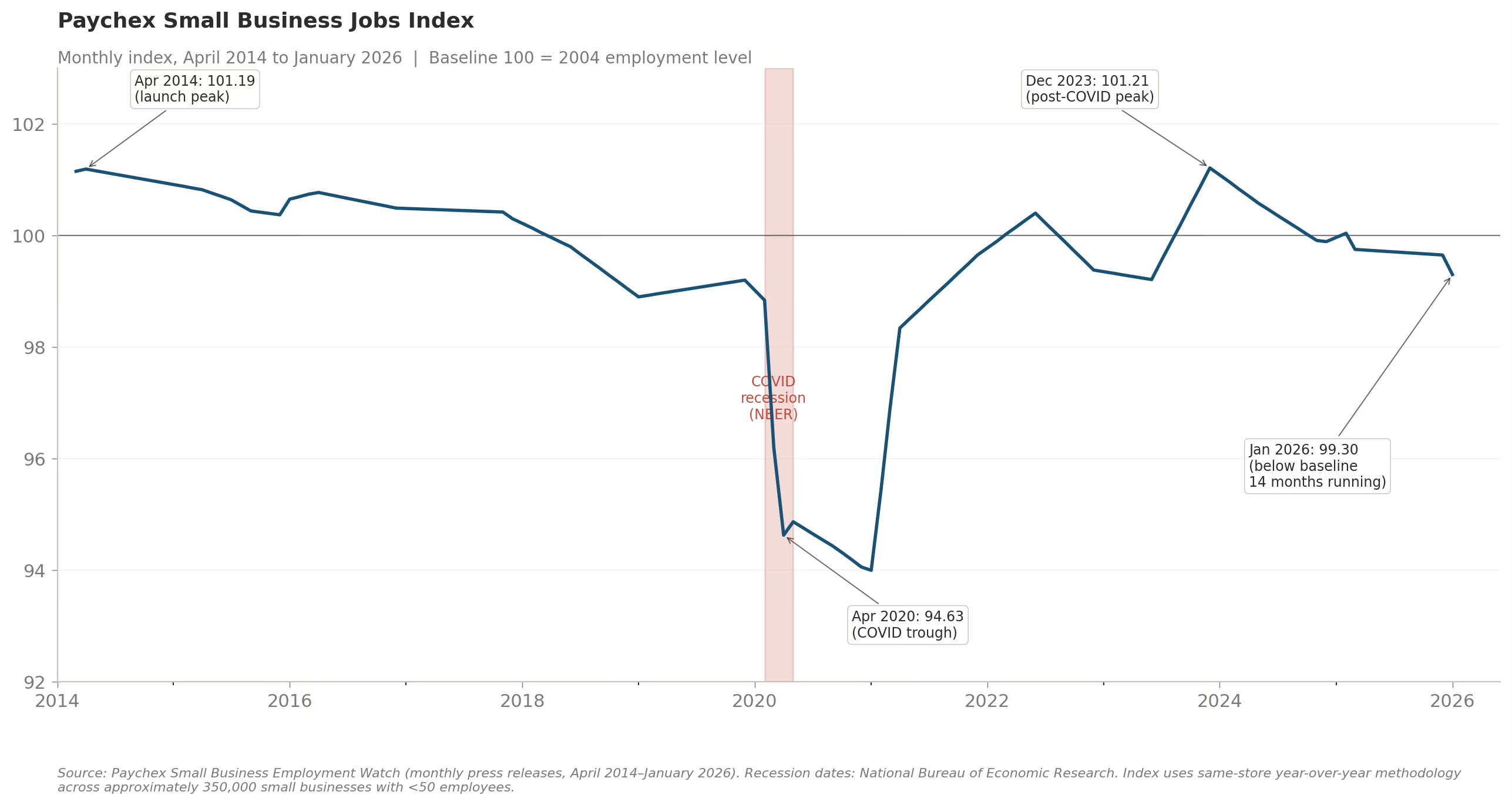

The Small Business Jobs Index Is Below 100

Paychex publishes its own Small Business Jobs Index. The SBJI baseline is 100.

It printed 99.30 in January 2026 and 98.81 in March. Below 100 means SMB employment is contracting on a relative basis.

Paychex revenue is partly priced per check. Fewer checks per client means less revenue. Yes, AI could increase layoffs at SMBs but the more immediate threat is a general economic contraction.

The SBJI is Paychex’s own data and based on their customers, but this is Paychex publicly warning that small businesses are getting hit by the current administration’s economic policies: tariffs, inflation, and high gas prices crimping the US consumer.

Things could change in the back half of the year, if tariff uncertainty dissipates, oil starts flowing through the Strait of Hormuz again, and inflation subsides enough to warrant further rate cuts.

Interest Rates

Paychex holds client funds between collection from the employer and disbursement to employees. Around $4.5 billion. Paychex gets to earn interest off this float at near-zero cost. It flows right to PAYX’s bottom line.

In FY25, interest was $167 million. In FY26, on management’s guidance, it’s tracking toward $205 million. Roughly 3% of total revenue and more than 3% of operating income.

Float income is rate-sensitive. Every 100 basis points of Fed cuts compresses the yield Paychex earns on those funds by approximately the same amount. Rates fall, float income declines, and earnings decline.

The operating-business EPS and the reported-EPS line have moved together for four years because rates have been a tailwind. But that has changed recently, and if the new Fed chief Warsh can get the board to lower rates further, then that is another earnings drag.

This is cyclical, and Paychex has been through many different rate environments, but a rate-cutting cycle occurring when market participants are pricing in business disruption increases the pressure on PAYX’s stock price.

What’s Priced In?

When I run a basic reverse DCF on Paychex at its current price, with a 9% discount rate and a 2.5% terminal growth rate, the market is pricing in roughly a 3.7% revenue CAGR with flat margins. Or if I keep revenue growth flat, it’s pricing in 650 basis points of margin compression.

Either way, the multiple has rerated to a slow-growing cyclical with float headwind and modest competitive erosion business.

The bears arguing AI is killing Paychex are over-arguing the case. The market doesn’t need that to be true. It only needs small business contraction and falling interest rates to play out, which looks to be the case, to justify the rerating of Paychex.

The bull counter is in the next 6-12 months SBJI inflects above 100 and the Fed pauses cuts, this could cause the multiple to snap back because the regulatory moat is durable. The PEO cross-sell flywheel kicks back in post Paycor acquisition. And now that 3.7% implied growth is too low.

The Real Threat

The SaaSpocalypse and AI disruption narrative is the loudest narrative, and it’s affecting Paychex’s stock price, but it’s not the immediate threat to Paychex’s core business.

It’s increased payroll processing competition on the low end, economic pressure on Paychex’s core small business customers, and declining float income in a rate-cutting cycle.