A Fading Morningstar (MORN)?

Is Morningstar a quality trap or a sentiment driven mispriced high-returning business.

The Charlie Munger 200-week moving average screen is supposed to help find high-quality companies trading at a discount, where short-term sentiment does not reflect the business’s long-term earning power.

But like all value-focused screens, it will also surface value traps, or in this case, quality traps: businesses whose returns look great in the rearview mirror but whose future is slowly eroding.

The name that popped out on a recent run of that screen, and that struck me as a potential quality trap, is Morningstar (MORN) because it is facing two secular changes that should negatively affect its business.

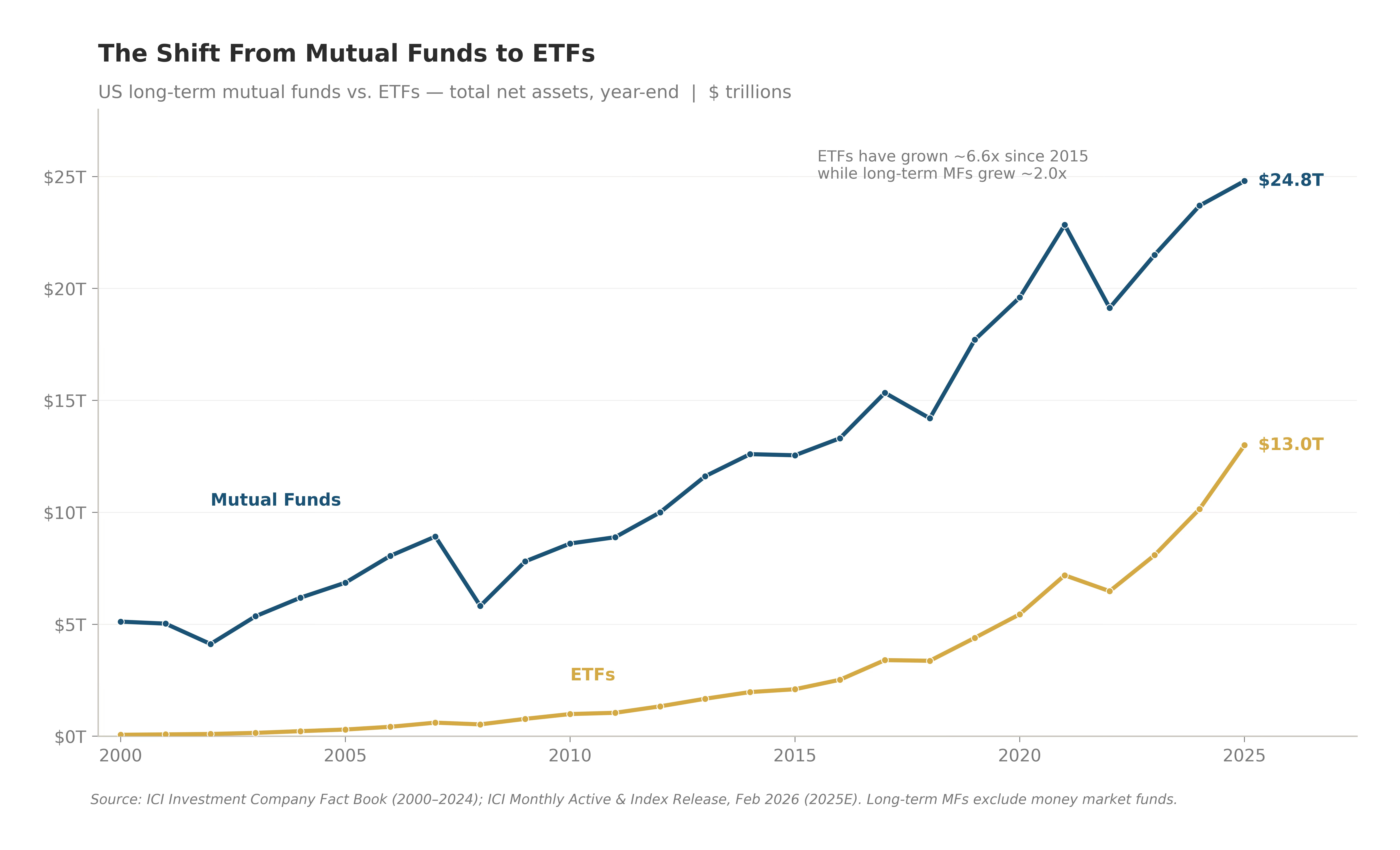

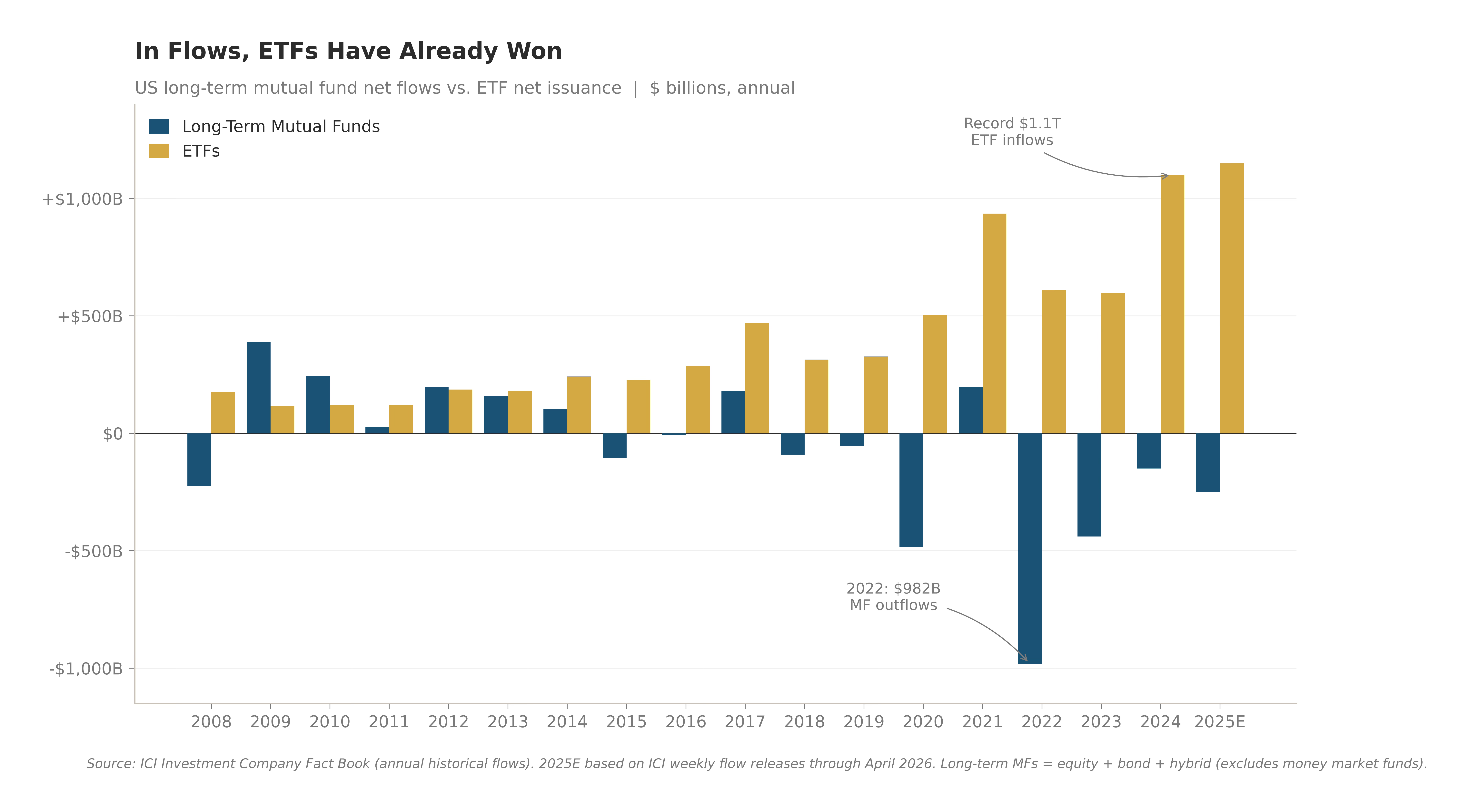

The first has been grinding away for a decade: the migration from active mutual funds to passive ETFs, which cuts at the heart of Morningstar’s original franchise.

On a assets basis it looks gradual but when you look at flows, the secular shift is more pronounced.

Since 2015, long-term mutual funds have had net outflows in most years. Since 2020, those outflows have run in the hundreds of billions annually.

ETFs, meanwhile, have pulled in positive flows every year, hitting a record $1.1T in 2024.

Active mutual funds are a shrinking pool, losing $250–500B a year. The main things propping them up are market appreciation and 401(k) plans.

Morningstar is synonymous with mutual funds.

It famously started in 1984 at Joe Mansueto’s kitchen table to fill a void and provide institutional-quality research on mutual funds. Any business built on the rise of mutual funds should show signs of deterioration as mutual funds decline in popularity.

The second threat is generative AI and its potential to commoditize the kind of packaged research and data that Morningstar sells. That threat is the reason MORN used to trade at 36.6× EBITDA in early 2024 but now sits at ~10.5× today, a multiple last seen during the GFC.

I worked in labs throughout college because I originally planned to become a scientist. That obviously did not happen, but the scientific method is ingrained in my thinking. So, like any good scientific endeavor, the goal here is to try to disprove my hypothesis.

If I can’t, then the Munger screen might have surfaced exactly what it was supposed to: a high-quality company experiencing undue negative short-term sentiment relative to its long-term earning power.

The cleanest way to run this test is segment by segment. Morningstar reports five segments today — Morningstar Direct Platform, PitchBook, Morningstar Credit, Morningstar Wealth, and Morningstar Retirement — plus an Indexes business sitting inside “Corporate and All Other” that just got a lot bigger and will probably become Morningstar’s sixth segment.

Morningstar Direct Platform

This is the segment people mean when they say “Morningstar.” It includes Morningstar Data, Morningstar Direct, and Advisor Workstation. These are the data feeds and analytical platforms that sit on the desktops of financial advisors and institutional analysts.

At roughly $820M of annual revenue, it is the largest segment. On paper, it is also the most exposed to both threats: the mutual fund database was built for an active-management world, and the GUI-based research workflow is exactly what an LLM should disrupt first.

So is it melting?

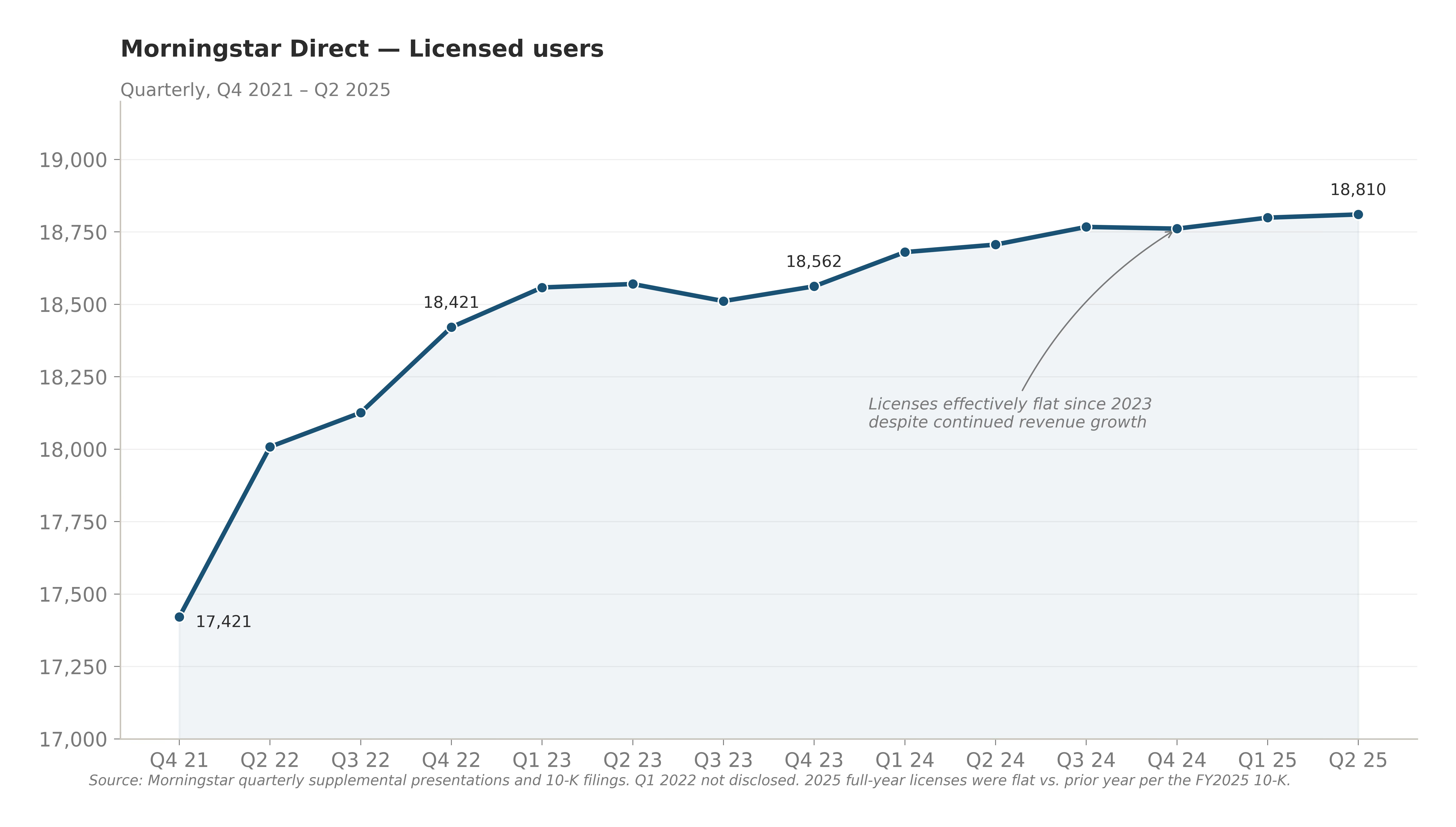

The first place to look is seats. Morningstar Direct licensed users are disclosed quarterly in the supplementals.

Direct licenses grew from ~17,421 at the end of 2021 to 18,562 by late 2023. Since then, growth has essentially gone flat. Over the next six quarters, users increased from 18,562 to 18,810.

If AI were going to strangle anything at Morningstar, it would start here, and the flattening licensed-user curve supports that story.

The AI threat is less about churn and existing users leaving to build their own solutions. It is more about slowing new customer acquisition, and the renewal rates support that.

In 2025, Morningstar Direct posted net retention of ~104% and Morningstar Data posted ~101%. Above 100% net retention means existing customers expanded contract value net of any churn.

Institutional data platforms in finance have always been workflow-sticky. Compliance-bound clients are slow to rip out incumbent systems, templates are embedded in downstream reporting, and Advisor Workstation in particular carries FINRA-reviewed audit trails that ChatGPT cannot replicate.

What the chart shows is Morningstar holding on tightly to existing customers while struggling to add new licensed seats. It is not just about AI. Last year was also a tough budget environment, and that showed up across several companies that serve the financial industry.

Right now, it is a decelerating business, not a melting one.

It is also what you would expect from a mature-category leader. Price protection and unit economics remain strong, but the top of the funnel gets harder.

Morningstar ≠ Mutual Funds

The idea that Morningstar is a mutual fund business misunderstands what Morningstar actually sells.

Morningstar’s customer is not the mutual fund investor. It is the financial professional who needs to analyze investments of any structure.

An advisor building a client portfolio in 2026 still has to compare expense ratios, holdings, factor exposures, tracking error, and historical performance. The advisor is agnostic to whether the asset is a mutual fund or an ETF.

It is easy to see why the decline of mutual funds did not coincide with the decline of Morningstar’s core business.

Morningstar Indexes

As we’ll see in the other segments, Morningstar’s management has a track record of recognizing where the business is headed, investing heavily in the right areas, and exiting the wrong ones.

They know ETFs are the future, and they have used their brand recognition to enter the index and ETF business.

So far, it has been a slow rollout. Morningstar Indexes is still reported inside “Corporate and All Other”.

But they just made a major investment with the acquisition of CRSP, and it should get its own reporting segment soon.

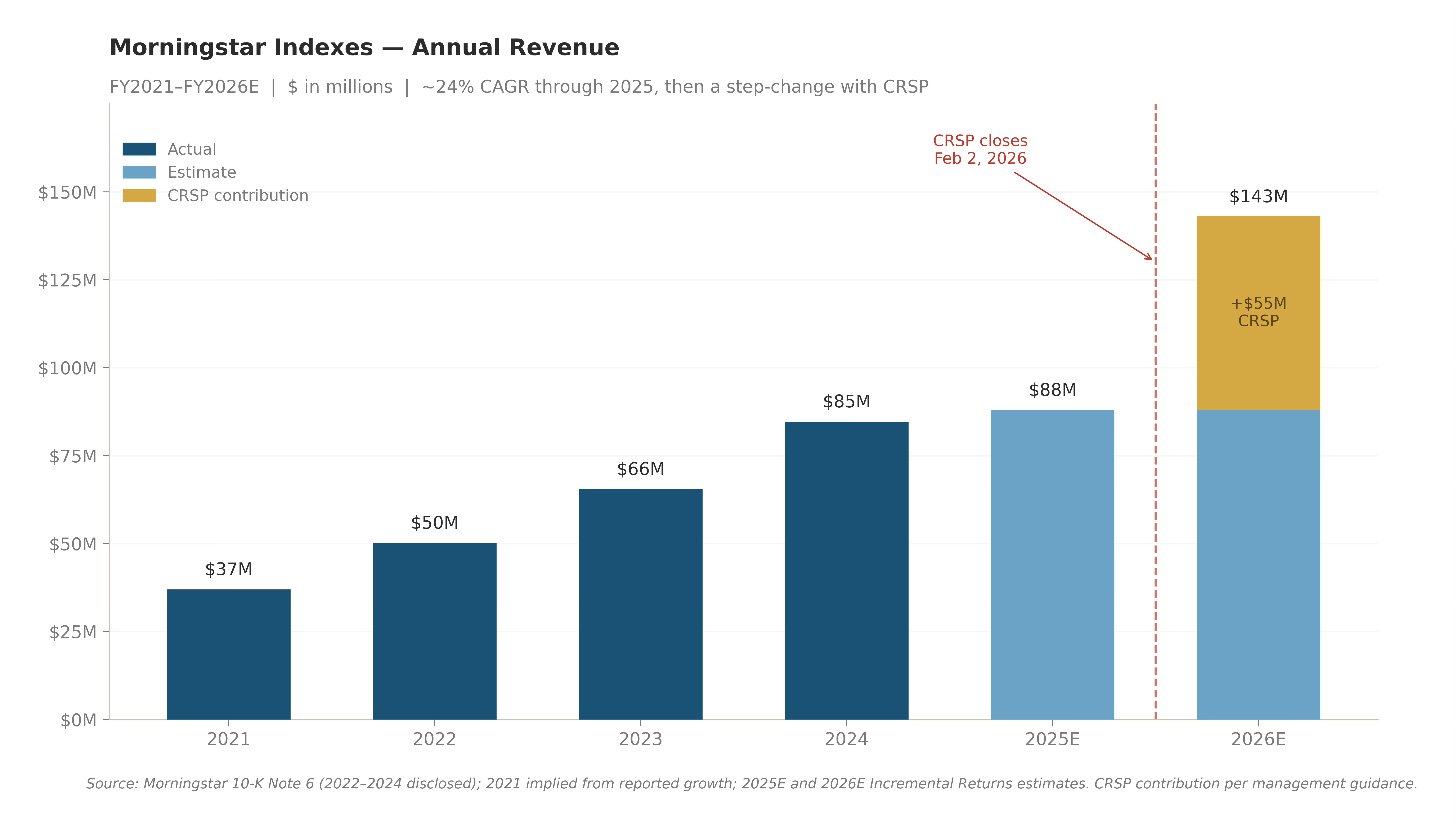

Morningstar Indexes revenue compounded from $37M in 2021 to ~$88M in 2025 before the CRSP acquisition. Then, in February 2026, Morningstar closed the $365M acquisition of CRSP, the University of Chicago-affiliated index provider whose US Total Market Index is the benchmark the Vanguard Total Stock Market Index Fund (~$2T AUM) is contractually required to track.

On a pro forma 2026E basis, the Indexes business jumps to roughly $143M, a ~60% revenue bump.

That growth is meaningful, but the acquisition also reshapes the competitive landscape.

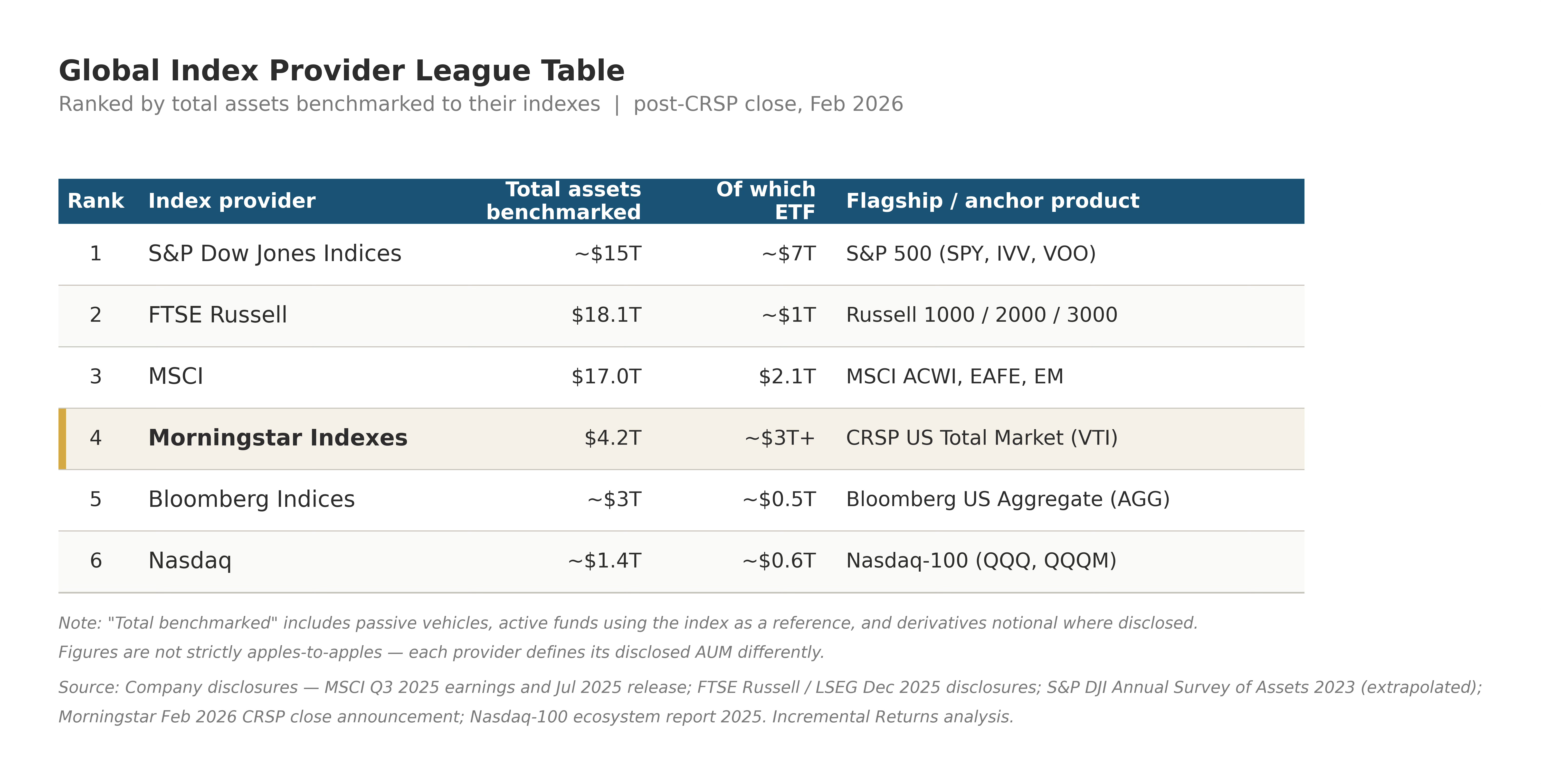

Morningstar Indexes went from a subscale also-ran to #4 globally, with $4.2T of assets benchmarked.

Of that $4.2T, roughly $3T+ is already in ETFs, which is a higher ETF share than every other provider in the table except S&P Dow Jones.

The segment is not without risk.

Vanguard is now the single largest client relationship inside Morningstar Indexes, and it is a famously price-sensitive counterparty. Vanguard left S&P for CRSP in 2012 specifically over pricing. The renewed multi-year license is reassuring, but it is not permanent, and future Vanguard renegotiations will be the most-watched events in this segment.

Management knows the future is ETFs, and it needed to become a bigger player in the space. The acquisition of CRSP, and the resulting Vanguard relationship, is a huge win and a smart investment.

Granted, the immediate revenue contribution from Indexes post-CRSP acquisition is still small at 5.7%. But the margin contribution is much higher. MSCI’s index business runs 75% adjusted EBITDA margins, and if Morningstar’s Indexes is similar, that implies about $110M in segment profit and roughly 15% of total EBITDA.

PitchBook

PitchBook is the key segment that determines whether MORN is interesting or not. It’s the private-markets intelligence platform Morningstar bought in 2016.

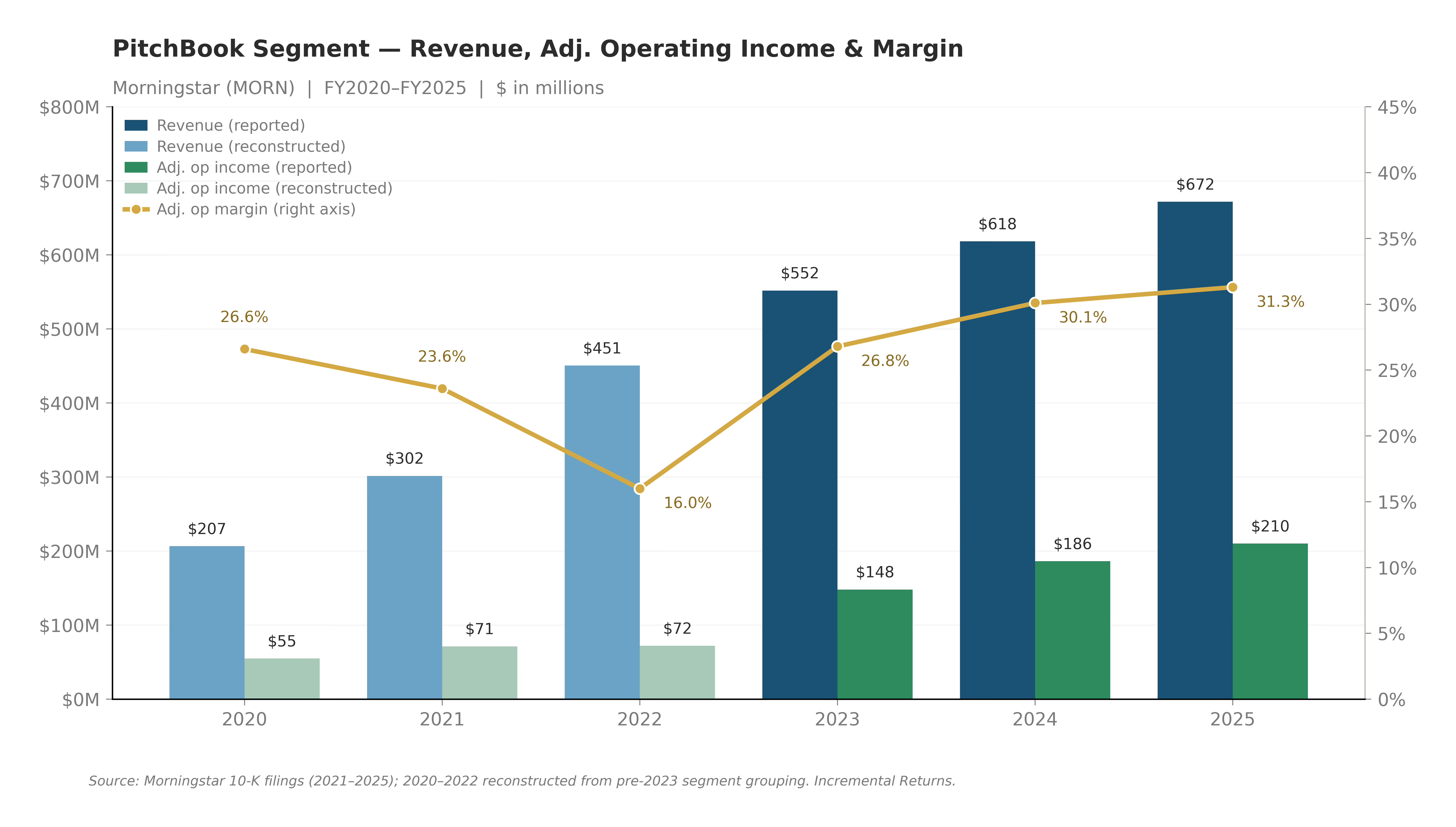

Revenue grew from ~$207M in 2020 to $672M in 2025 — roughly 3.2× over five years — while adjusted operating margins moved from 26.6%, down to a 2022 investment-cycle trough of 16.0%, and back up to 31.3% in 2025.

Adjusted operating income went from $55M to $210M over the same window, nearly 4×. Even with growth decelerating, the profitability curve is moving in the right direction. Margins are expanding, not compressing, which is the opposite of what you’d expect from a business being commoditized.

The AI disruption narrative has the most superficial appeal with PitchBook because it is the closest thing Morningstar has to a “research portal” product.

But PitchBook’s value isn’t the UI. It’s the database behind it.

Decades of accumulated deal data, fund-level returns, LP commitments, portfolio company financials, and league tables. Private-markets data is not on the open web. An LLM cannot scrape it because it was never posted. It has to be sourced, verified, and maintained the way PitchBook has been doing since the mid-2000s. So when a new AI-native application needs canonical private-markets data, whose data does the AI call?

Management has been active in making sure that call goes to PitchBook. They’ve signed data and distribution partnerships with OpenAI, Anthropic, Microsoft, and most recently, Perplexity.

PitchBook is also rolling out MCP servers and AI APIs for generative summaries and model connectivity.

Morningstar is also trying to turn PitchBook from just a private-markets database into a broader research platform by adding more asset classes and analytical layers.

They’ve added analyst-driven public equity research to the database. It also aggregates third-party research from nine outside partners.

Morningstar bought Leverage Commentary & Data (LCD) from S&P in 2022. This brings leveraged loan and high yield bond data into PitchBook Credit. They also bought Lumonic to improve portfolio monitoring of credit positions.

On top of distribution deals with top AI companies, PitchBook is adding its own AI research layer, PitchBook Navigator.

The problem is that all this investment and expansion has not changed PitchBook’s revenue deceleration.

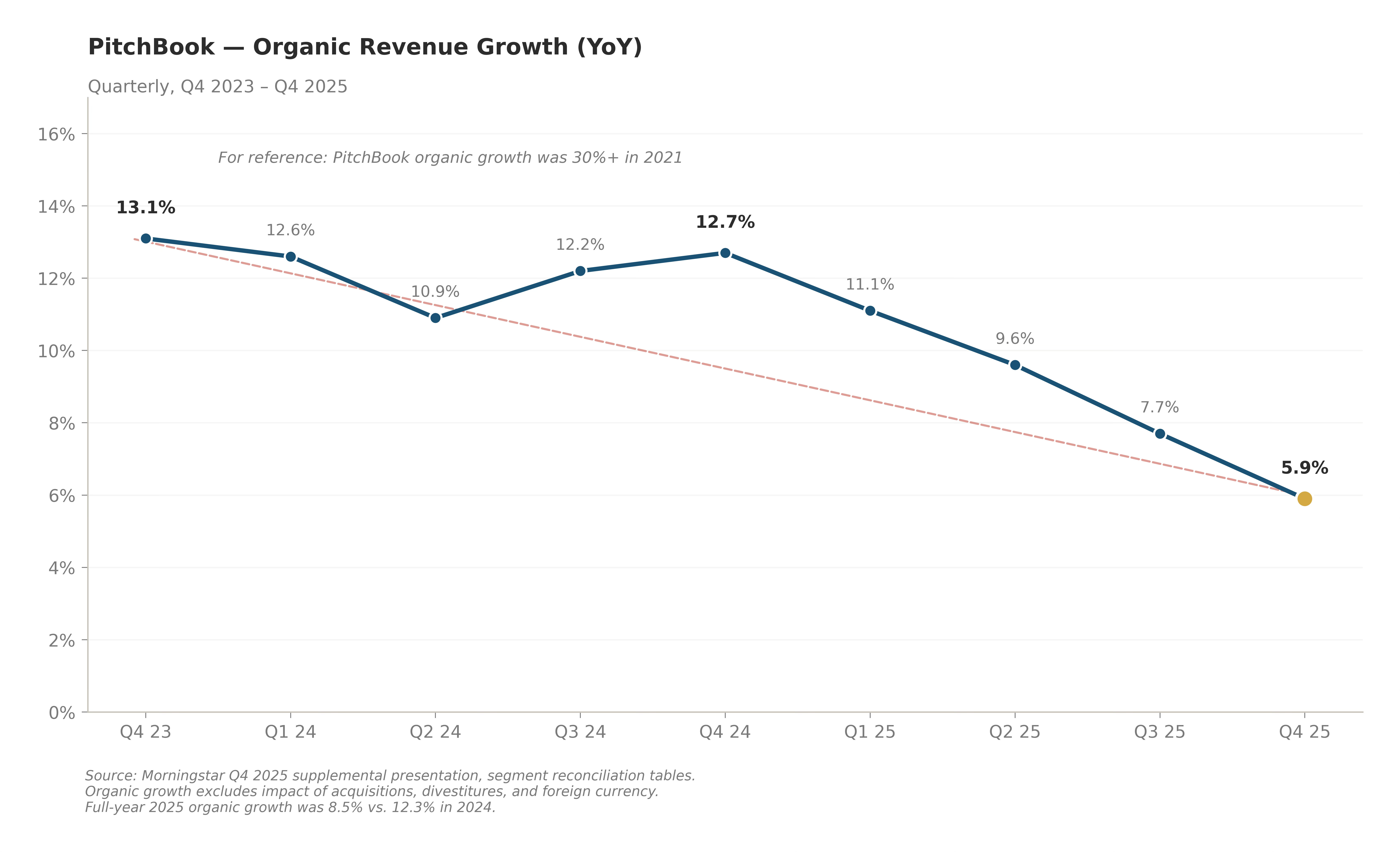

PitchBook’s organic growth decelerated from 30%+ in 2021 to 8.5% in 2025, and Q4 2025 came in at just 5.9% organic, the lowest quarter in the dataset.

Licensed user count was essentially flat in 2025 at 113,447 versus 113,451 the year before. To be fair, there was a methodology change in how users were counted (internal active users were removed from the count), but it is still a caution sign.

The combined PitchBook platform & direct data renewal rate also ticked down from 108% in 2024 to 103% in 2025.

I see two reasons for this.

The platform expansion is aimed at deepening wallet share with core investor/advisor clients, which pushes out smaller users and increases churn.

The easy upsell to current clients is gone. This is, again, a new user acquisition issue.

Either PitchBook is settling into a normal mature-SaaS growth rate (high single digits), with AI partnerships reaccelerating it as the distribution deals compound, or PitchBook is structurally breaking and heading for sub-5% organic growth as AI alternatives pick at the edges.

The next four quarters are important.

If PitchBook reaccelerates even modestly, the whole MORN thesis gets materially easier. If it slips further, the bear case on the stock gets a lot more credible.

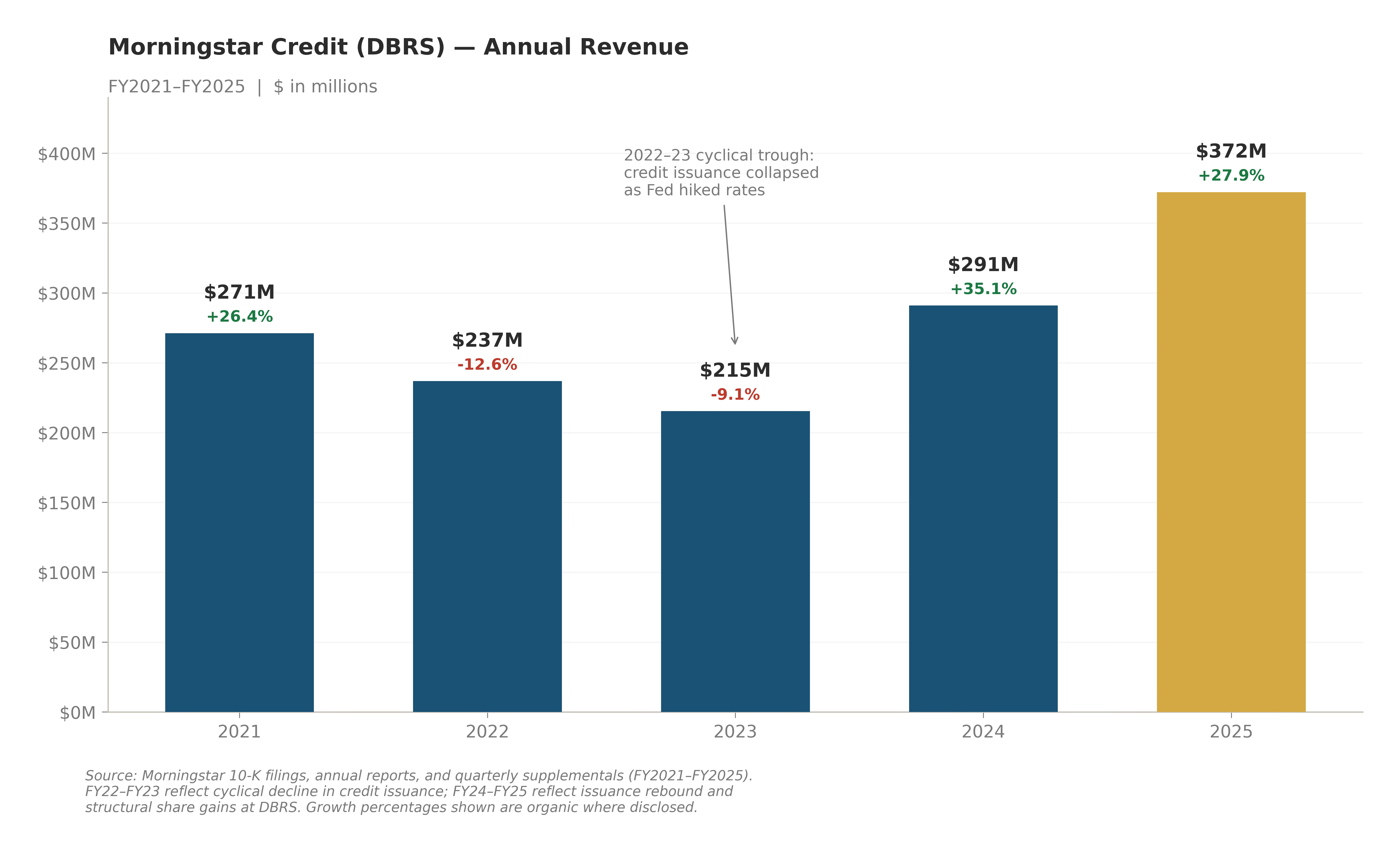

Morningstar Credit (DBRS)

Morningstar Credit is essentially DBRS, the fourth-largest credit rating agency in the world, plus Morningstar Credit Analytics.

It is one of roughly ten SEC-registered nationally recognized statistical rating organizations (NRSROs), and one of only four credit rating agencies the ECB recognizes as an external credit assessment institution. The other three are S&P, Moody’s, and Fitch.

An LLM cannot assign an NRSRO-recognized credit rating. No issuer is going to structure a CLO around ChatGPT’s or Anthropic’s credit opinion, because the regulatory framework that governs CLO tranching, bank capital treatment, insurance-company investment mandates, and a dozen other downstream uses of credit ratings requires a recognized, licensed rating from an approved body. The cost of entry is enormous: multi-year track record requirements, jurisdictional approvals, and issuer inertia. The list of approved bodies is essentially closed.

And the business itself has just come ripping out of a cyclical trough.

Credit revenue peaked at $271M in 2021, then fell for two straight years as the Fed hiked rates and CMBS / RMBS issuance collapsed.

Then the cycle turned.

This segment grew revenue 35.1% in 2024 and another 27.9% in 2025. It was the fastest-growing Morningstar segment for two years running. The growth was driven by strength in corporate ratings globally and structured finance ratings in the US and Europe.

DBRS has been taking share steadily for years by positioning itself as a credible “diversity alternative” to the big three. Post-2008, issuers have a structural incentive to get a second or third rating from a non-big-three agency for capital-markets-access reasons.

DBRS is the least likely business division to be disrupted by AI.

Morningstar Wealth

Morningstar Wealth was historically a TAMP (turnkey asset management platform) business, offering model portfolios and SMAs for financial advisors.

Full-year 2025 revenue was roughly flat, and adjusted operating margins were in the low single digits.

This business is a melting ice cube.

Not because of AI or the secular shift to ETFs, but because it is a highly competitive industry where Morningstar has no meaningful advantage versus larger platforms like Envestnet.

Management recognizes this and is unwinding the business. Through 2024 and 2025, Morningstar has been sunsetting TAMP assets and booking some gains on sales.

Morningstar Wealth is small (~$255M of revenue, roughly 10% of the company), and eliminating the drag is accretive to consolidated margins. Removing the Wealth drag could add another 100–200 bps to Morningstar’s consolidated adjusted operating margin.

Morningstar Retirement

Morningstar Retirement is the smallest segment, at roughly $125M in revenue, with mid-40s adjusted operating margins and mid-single-digit growth.

Morningstar Retirement sells managed-account and fiduciary services to 401(k) plans. It sits on top of employer-sponsored retirement plans and provides personalized allocation advice to participants. Revenue is asset-based and scales with market levels and participant adoption.

There is not much of a disruption story here.

The business is protected by regulation (managed accounts carry fiduciary responsibility, which consumer AI tools do not), the customer base is sticky (plan sponsors rarely switch recordkeepers because it is operationally painful), and the growth driver is plan-level participant adoption that compounds quietly.

What Expectations are Priced In?

There are no bad assets, only bad prices.

- Howard Marks

The final piece is what expectations the market is pricing in. If expectations are too pessimistic, then Morningstar could be a buy even if some AI disruption occurs.