Microsoft: Bull vs Bear

TCI and Egerton see the AI race slipping away. Ackman sees a mispriced fortress. I lay out both sides and where I sit.

TCI cut Microsoft from 10% of the portfolio to 1% in the first quarter, and it’s probably at 0% by now.

Egerton Capital, a woefully underfollowed fund, fully exited its position too.

Meanwhile, Bill Ackman initiated a brand-new ~$2.1 billion MSFT position.

Three concentrated, high-conviction stock pickers came to opposite conclusions in the same quarter.

TCI and Egerton see Microsoft losing the AI race. Ackman sees a fortress that’s mispriced.

The Bear Case: “AI Introduces Uncertainty Over Microsoft’s Competitive Position”

Chris Hohn was explicit in TCI’s Q1 2026 investor letter:

“We reduced our investment in Microsoft because the rapid progress in AI introduces uncertainty over Microsoft’s competitive position in the future.”

He singled out two specific concerns: the Office productivity franchise, and what he called “some risks in Azure.”

TCI then redeployed the capital from MSFT into Alphabet. Raising it to 5% of the portfolio and making it their largest tech position.

TCI rode Microsoft through a near-400% return over nine years. So when a high-conviction, long-term holder sells the position completely, you have to stop and ask: what do they see? Especially when MSFT is part of your own portfolio.

Productivity

The bear case on Office isn’t that ChatGPT, Claude, or other LLMs replace Word or Excel. It’s that AI-native productivity tools chip away at the Office bundle one workflow at a time. The bundle has been Microsoft’s moat for 25+ years. If AI-native tools fragment the workflow, its not one death blow but a death by a thousand cuts.

Recent data points have been unpleasant.

Microsoft 365 Copilot’s Net Promoter Score landed at -19.8 in early 2026 and it’s market share among paid AI subscribers collapsed from 18.8% to 11.5% in six months. And after more than 18 months on the market, Copilot sits at roughly 20 million paid seats. That’s about 4% penetration of the M365 installed base. Seat additions are accelerating. The most recent quarter was the fastest net-add quarter since launch, but the absolute share losses is showing up in the data.

“Just bolt AI onto the legacy suite” isn’t a winning product strategy. And I think that’s what Hohn believes MSFT’s strategy is right now.

“Some Risks” in Azure

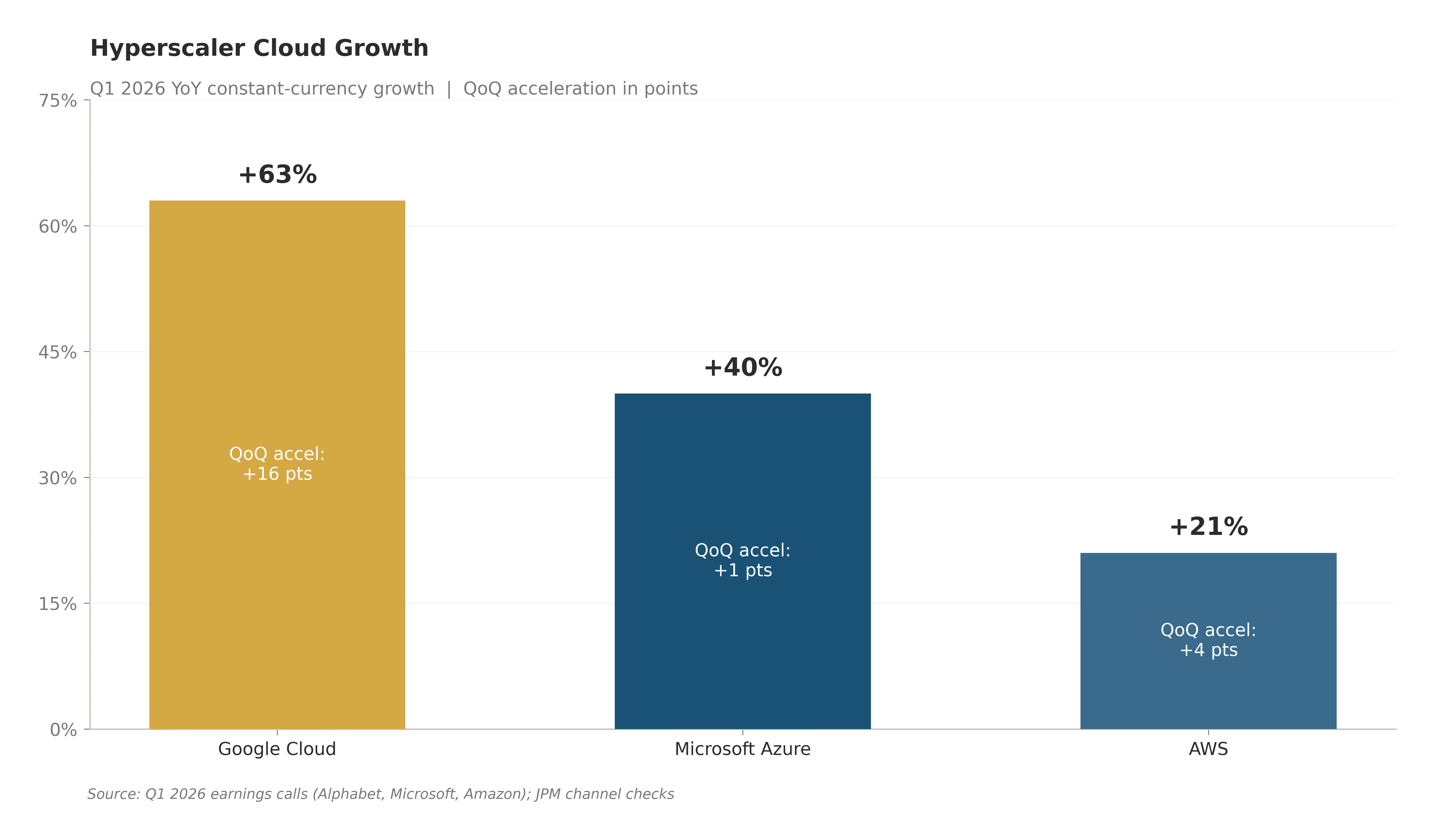

Hohn didn’t elaborate on Azure, but it might be the growth rate and the quality of its CRPO backlog.

Google Cloud grew 63% year-over-year in Q1 and accelerated 16 points sequentially. AWS grew roughly 21% and accelerated 4 points. Azure grew 40% in constant currency and accelerated 1 point. All three hyperscalers are running faster, but Azure is running the slowest right now.

For roughly a year, Azure has been range-bound between 35–39% constant-currency growth—which, don’t get me wrong, is still great. But the narrative was always “Azure is the AI cloud.” If that’s the case, then its growth rate should’ve shown up stronger this quarter when all the other hyperscalers’ growth rates picked up. But it didn’t.

Microsoft’s guidance for the next quarter calls for modest acceleration, supported by capacity coming online roughly six weeks earlier than expected at the Fairwater, Wisconsin facility. So they are still capacity constrained, not demand constrained. But this is the third quarter where MSFT has said “we couldn’t keep up with demand,” and at some point investors stop accepting it.

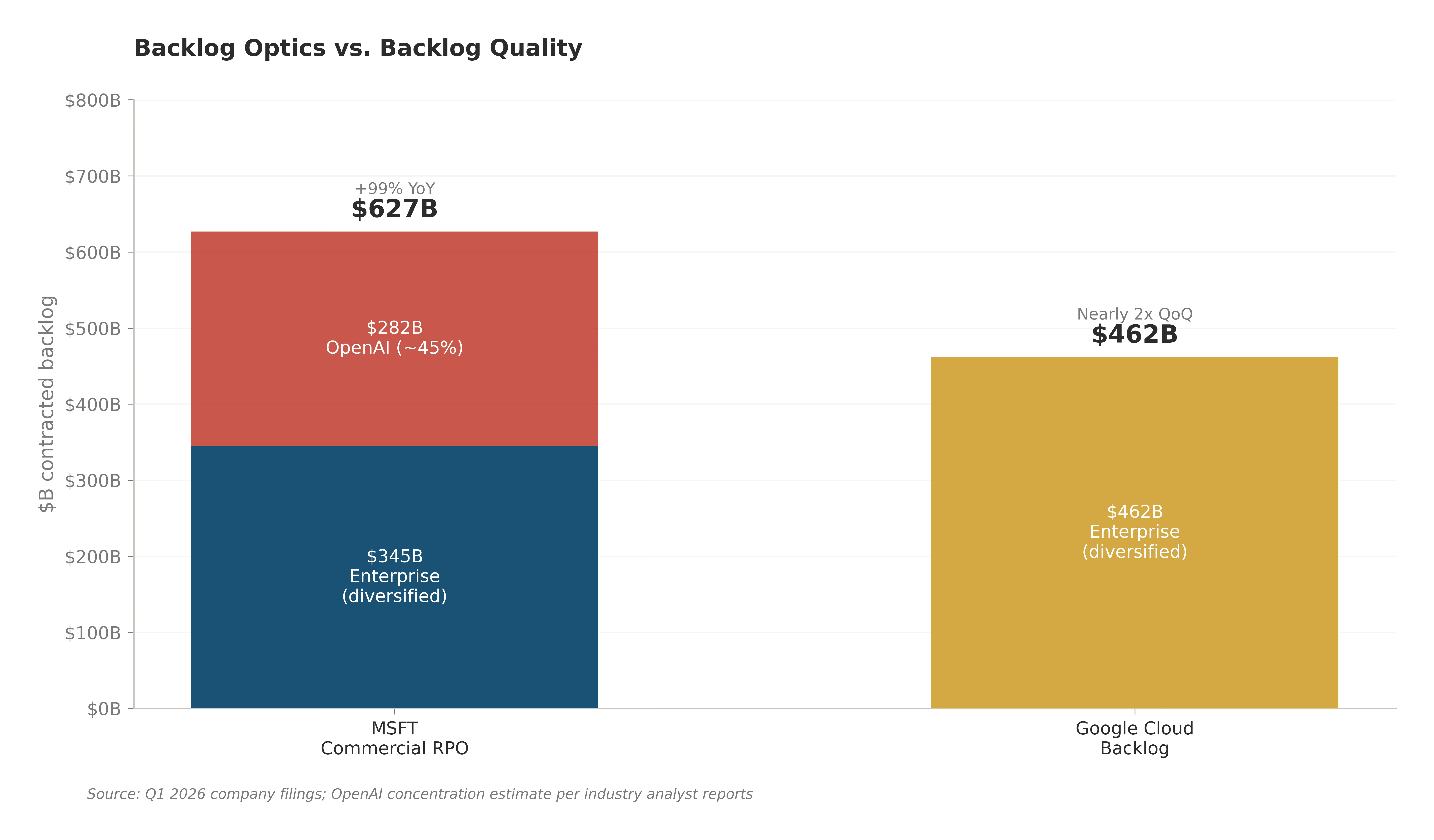

The quality of MSFT’s backlog could also be a concern.

Microsoft’s Commercial Remaining Performance Obligation is $627 billion, up 99% year-over-year and bigger than Google Cloud’s $462 billion backlog. But size isn’t the same as quality. Roughly 45% of Microsoft’s CRPO is concentrated in OpenAI commitments. Google’s backlog is more broadly distributed across enterprise customers.

The workload mix is probably Microsoft’s most defensible point.

Google Cloud is winning AI training workloads thanks to TPUs and the native Gemini stack. Azure is winning enterprise AI inference layered onto existing M365 and identity infrastructure. This should be stickier with a higher-margin profile.

The growth gap is an interesting short-term data point, but Azure is also growing 40% off a base roughly 2.5x larger than Google Cloud’s. This is a risk to monitor, but not a thesis-breaker, yet. If Azure dips below 35% while GCP stays above 50% for two consecutive quarters, it becomes worrisome.

The Bull Case: The Fortress Is Mispriced

Ackman built his position in MSFT during the Q2 selloff. This continues a recent pattern: Alphabet during its “AI loser” panic, Amazon after Liberation Day, Meta during its capex panic, and now Microsoft on AI skepticism.

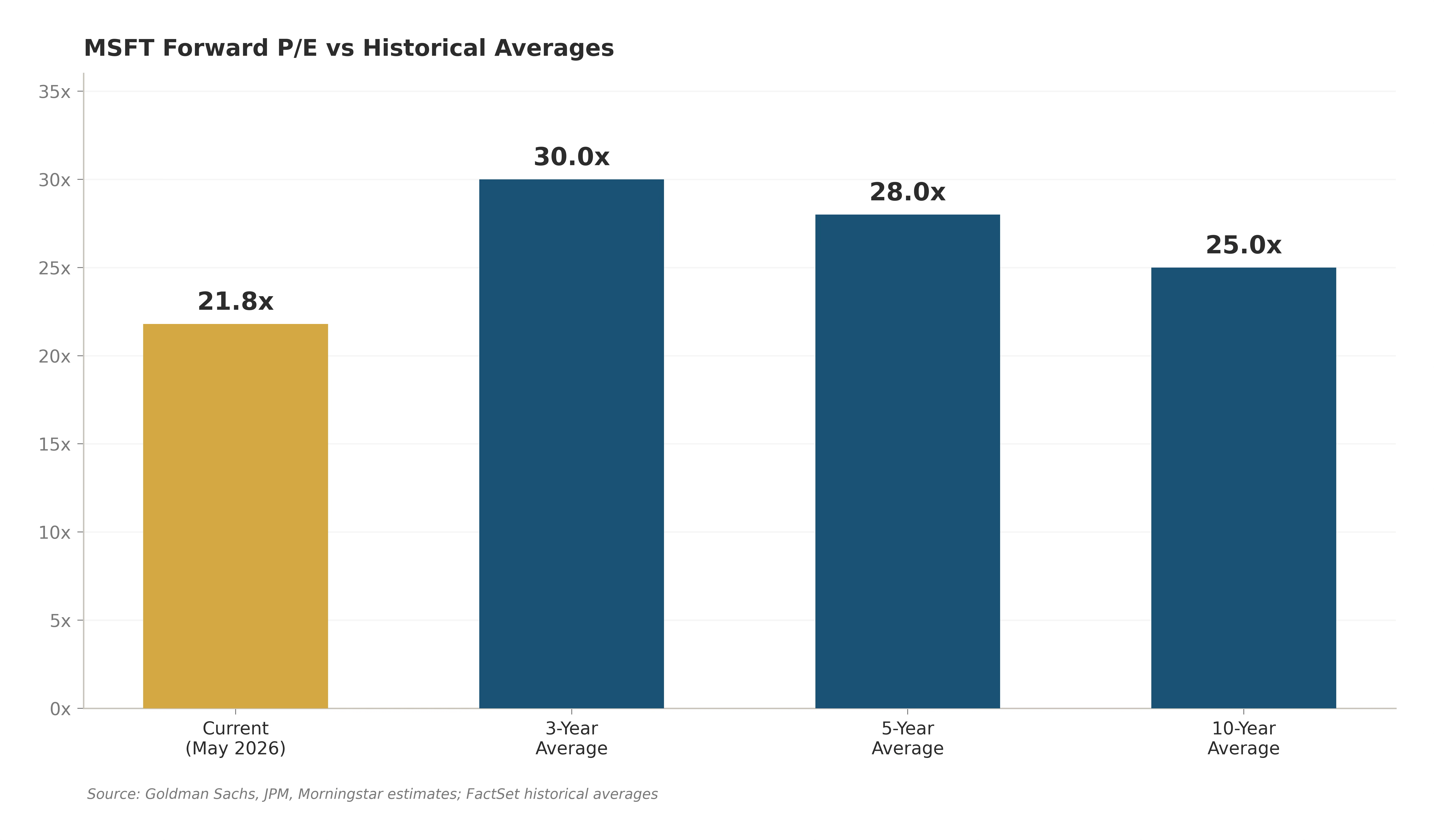

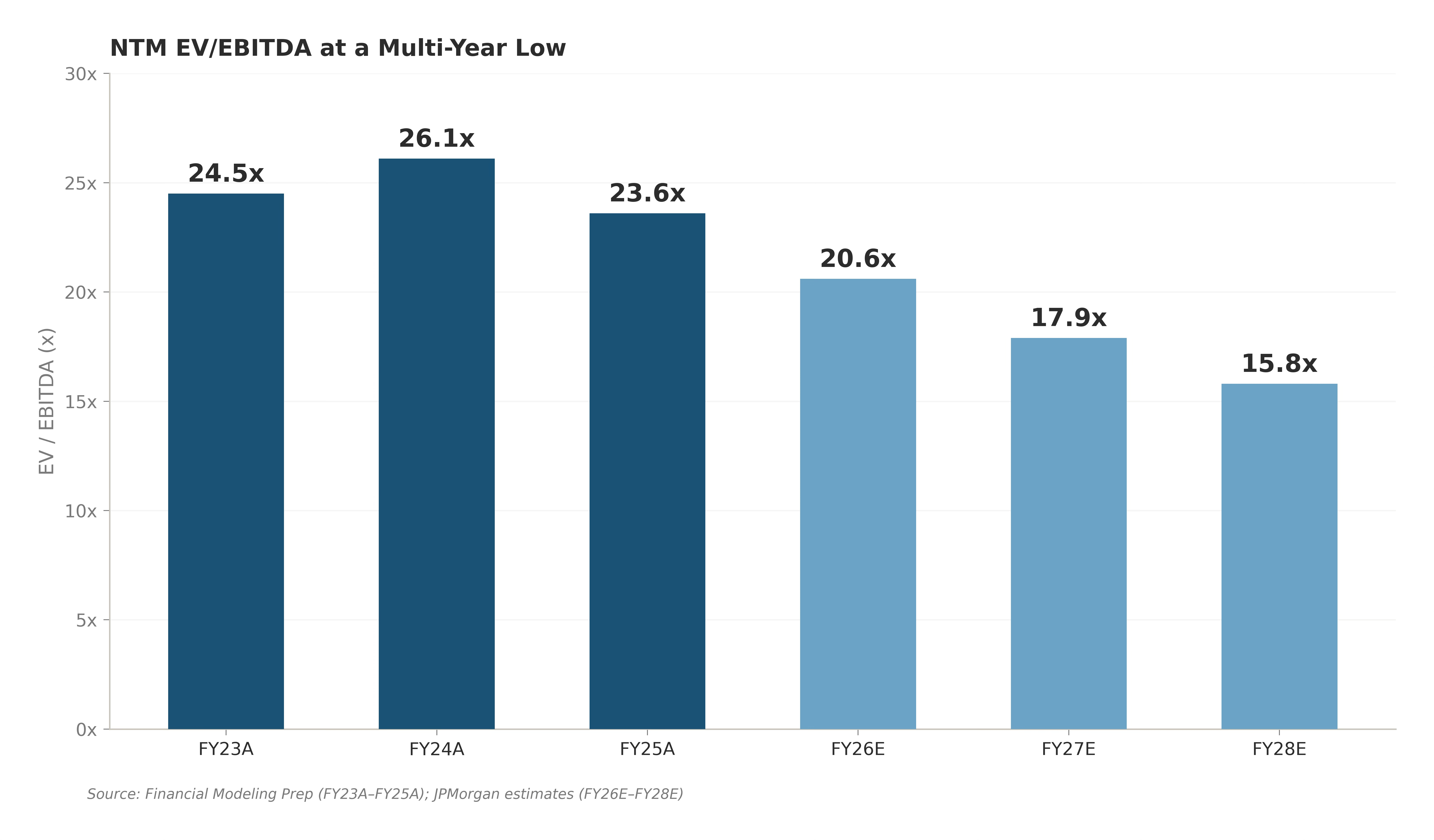

MSFT’s valuation is at a multi-year low.

At roughly 21x forward earnings, Microsoft trades in line with the S&P 500. This is below its own three-year average and at the bottom of its NTM EV/EBITDA range.

Buying the most dominant enterprise software franchise in the world at a market multiple has historically been a profitable trade.

The core of Ackman’s thesis is that M365 is a fortress.

Microsoft 365 isn’t a single application; it’s a bundle tied together with Microsoft’s security, compliance, and governance infrastructure. He describes it as “tightly integrated into the daily workflow of nearly every large enterprise.”

An AI startup can replicate Word. It cannot replicate years of embedded enterprise identity, authentication, and data-governance infrastructure. M365 and Office are the industry standard, the common language across businesses. Take Excel: it’s the common denominator across all of finance. LLMs like Claude aren’t trying to replace it; they’re trying to become a valuable tool within it.

The Copilot share-loss data is real, but it has mostly come from individual consumers, not enterprise, which really drives the economics. Claude and Excel work great together, and it’s what Copilot should’ve been from the start. It’s also why MSFT formally designated Anthropic as a sanctioned sub-processor for MSFT’s Online Services in early 2026.

Ackman also believes the market is mispricing MSFT’s OpenAI stake.

MSFT’s ~27% economic interest in OpenAI is worth roughly $200 billion at OpenAI’s most recent funding-round valuation. That’s roughly 7% of Microsoft’s current market cap. The total Microsoft investment across several rounds was roughly $13 billion. The stake is now worth approximately $228 billion. That’s a 17.6x return.

Ackman’s counter to recent worries about capex and cash flow is that MSFT’s current capex is in a classic J-curve.

Hyperscaler capex keeps ratcheting upward and MSFT’s FY26 capex is now expected to be $190 billion. But that’s $190B against $627B of contracted demand and an AI business running at a $37B annual run rate, up 123% year over year. Though frighteningly high, the capex looks like growth investment against visible demand, not speculative overbuild. The thesis breaks if demand declines.