Why Nobody Leaves LPL Financial

$2.4 trillion in assets, a 97% retention rate, and three stacked factors that make switching genuinely expensive.

LPL Financial ($LPLA) is the largest independent broker-dealer in the United States, supporting more than 32,000 financial advisors and roughly 11 million customer accounts, with about $2.4 trillion in advisory and brokerage assets on its platform at the end of 2025.

It is not an asset manager.

It provides the plumbing to independent advisors to run a modern wealth management practice: technology, clearing, custody, compliance, research, and practice-management support.

The bulk of its profits come from advisory fees, commissions, and interest on client cash.

Its dominant position is built on three main factors: immense switching costs, scale advantages, and barriers to entry.

Switching Costs

Switching costs are LPL Financial’s single strongest competitive advantage.

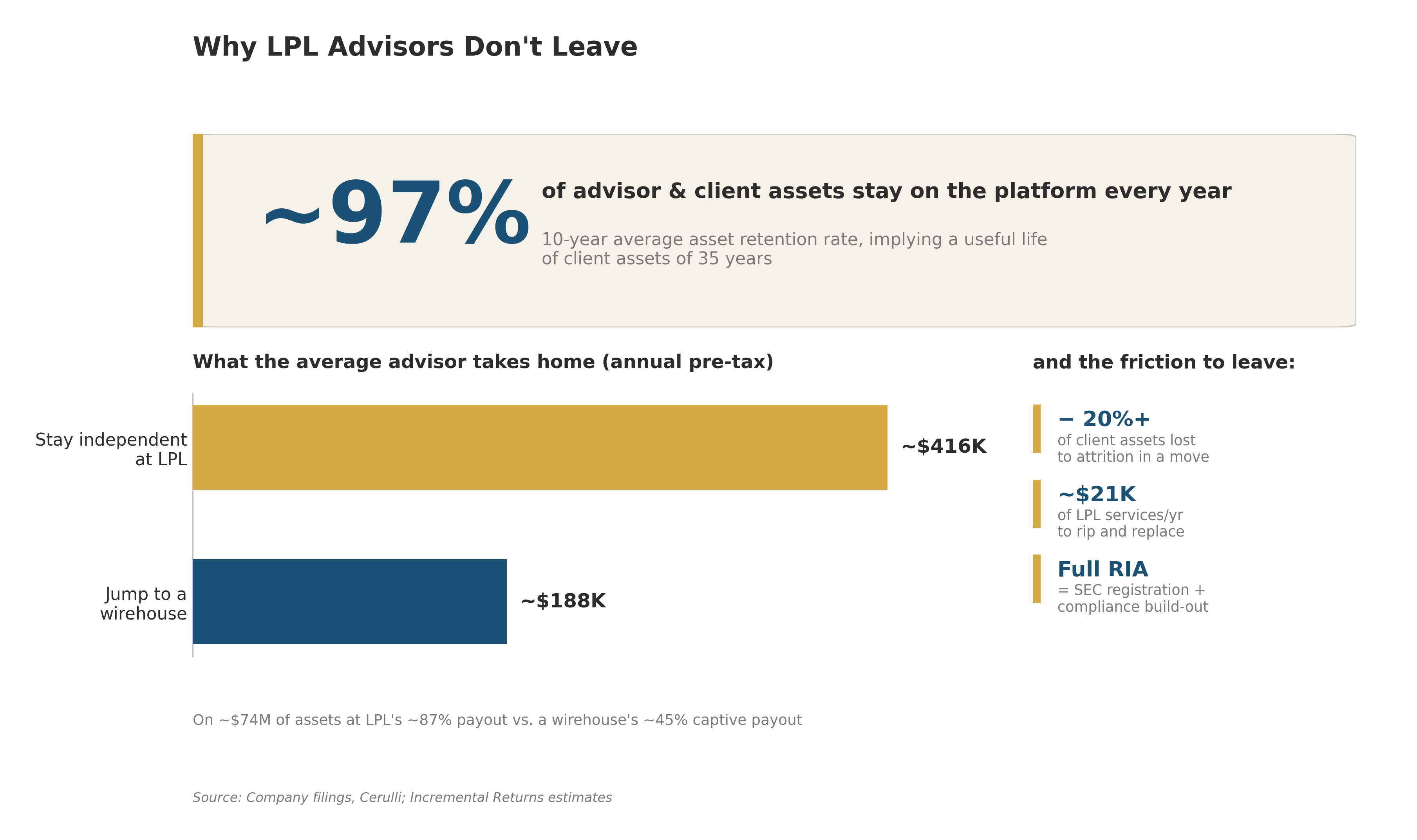

LPL has retained roughly 97% of platform assets on an average annual basis over the past decade. This translates into a useful life of client assets around 35 years.

Advisors and their clients, once on the platform, simply do not leave.

Why don’t they leave?

Because leaving is genuinely expensive, on several fronts.

The first cost is client attrition.

Industry data from Cerulli suggests that advisors who change firms lose upwards of 20% of their assets in the transition—clients who don’t want to make another move and accounts that fall through the cracks during repapering.

When your revenue and earnings are based on assets under management, losing clients is a large haircut to earnings and it could take years to replace those lost assets.

The second is the economics of the relationship.

LPL’s average advisor manages about $74 million in assets and generates roughly $470,000 in annual revenue. At LPL’s payout rate of nearly 87%, that advisor keeps around $416,000 before their own overhead. If that same advisor jumped to a wirehouse, where captive payouts cluster near 45%, they’d take home closer to $188,000. The independent model pays more than twice as much and a competitor would struggle to replicate those economics.

The third cost is operational entanglement.

LPL layers on roughly $21,000 per advisor of a la carte services. This includes marketing support, bookkeeping, paraplanning, integrated technology for running a practice. Leaving means an advisor would lose immediate access to this support harming how the business is ran and then they would have to spend time and money finding sourcing replacements from multiple vendors.

Leaving means an advisor would lose immediate access to this support, harming how the business is run, and then they would have to spend time and money sourcing replacements from multiple vendors.

And the only off-ramp that increases payouts is going fully independent as a registered investment advisor. But this means SEC registration and building a compliance and risk infrastructure from scratch. This is a daunting proposition for the typical advisor.

LPL even takes care of the most natural form of attrition, retirement. LPL has a liquidity and succession program that transitions retiring advisors’ books to other advisors and keeps the assets in-house.

All these stacked together create immense switching costs for an advisor.

Scale and Cost Advantage

As the largest independent broker-dealer in the country — after absorbing Commonwealth Financial Network — LPL spreads its fixed costs (technology, clearing infrastructure, back office) across a far larger base than any direct competitor.

Measured the same way a custodian like Schwab would report it, LPL’s expense on client assets runs around 0.20%, well below large banks such as Morgan Stanley (0.33%) and Bank of America (0.41%). Schwab’s is 0.11%. LPL is, in its own words, the lowest-cost solution for independent advisors on the market.

Taking a play book from Costco, LPL chooses to pass much of that scale benefit back to advisors in the form of industry-high payouts rather than keeping it as margin.

This is their flywheel: greater scale lowers the unit cost to serve each advisor, which funds the highest payouts in the business, which attracts and retains advisors, which adds scale.

The result over the past decade is an advisor headcount that has compounded at about 8.7% annually. Industry-wide advisor growth is roughly 0.3%. This means LPL is not only growing with the market but taking market share from competitors.

Passing these savings on through to its advisors instead of maximizing near-term profit, leaves little room for a well-capitalized competitor to undercut LPL. You might have to destroy your own economics to beat LPL on price.

Barriers to Entry

The barriers to entry in this business are high and rising.

There are a lot of regulations in this business. Operating a self-clearing broker-dealer and an RIA at national scale requires registration, net-capital reserves, and a compliance apparatus that is expensive to build and expensive to maintain.

Then there are financial barriers to compete. LPL reinvests north of $465 million a year into its technology platform, smaller independent broker-dealers cannot match this spend without eroding their profitability.

Probably the largest barrier is the economics of its advisor deals.

To lure LPL’s advisors away, a challenger would need to match LPL’s nearly 90% payout and its low cost base and its breadth of services. Smaller independent peers can’t afford the payout; wirehouses won’t cannibalize their captive model; and pure-play custodians like Schwab and Fidelity are aimed at a different customer. Meaningful encroachment on LPL’s core market looks unlikely, which is exactly why the firm keeps compounding share.

Network Effects

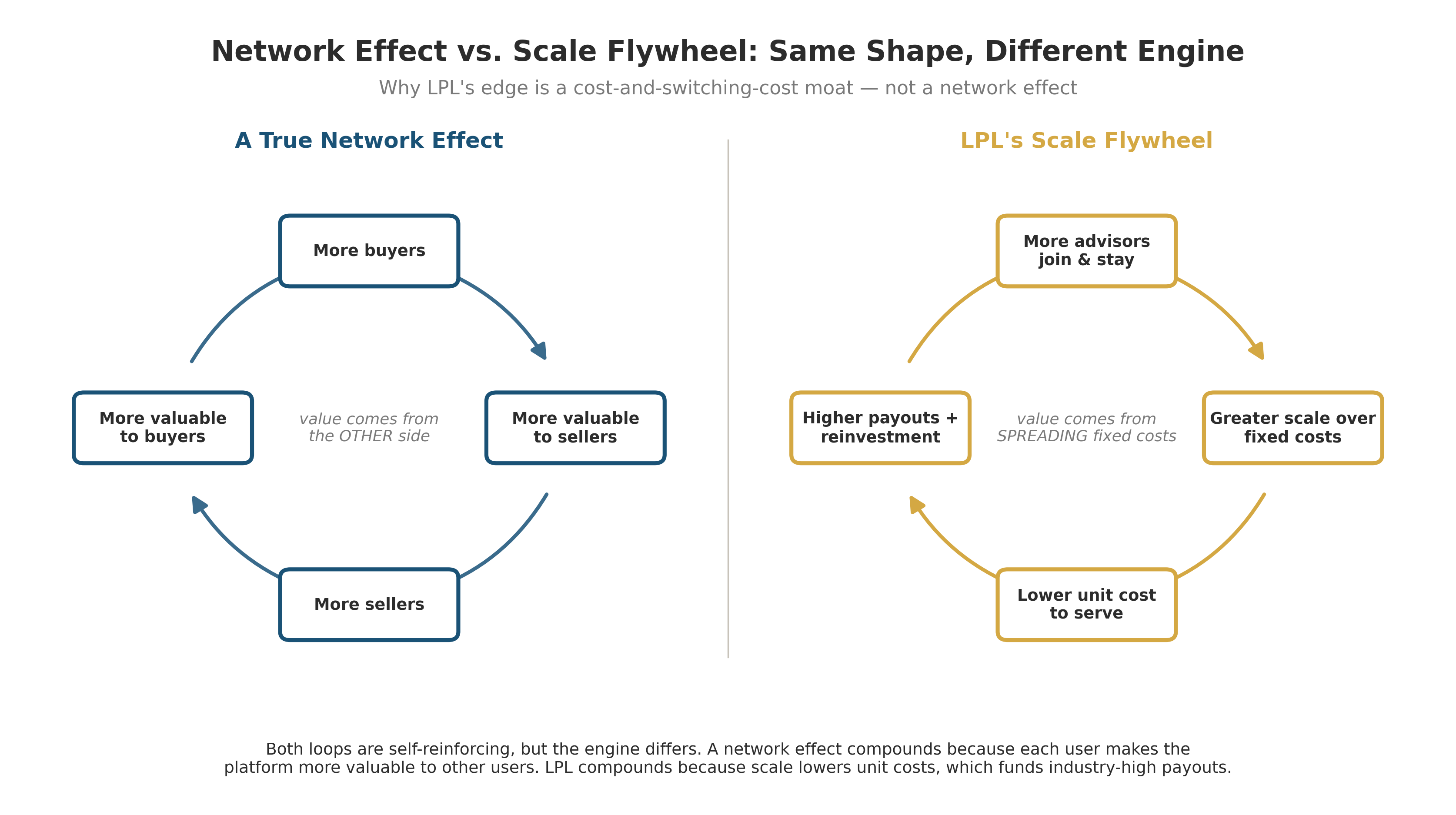

It’s tempting to describe LPL’s flywheel as a network effect, and you’ll see it called one, but it isn’t. The distinction matters for assessing the strength of its competitive factors.

A true network effect compounds because each new user makes the platform more valuable to other users. Think of a marketplace or an exchange, where more buyers attract more sellers, which attracts more buyers.

LPL doesn’t work that way. One advisor joining LPL doesn’t make the platform meaningfully more valuable to another advisor; advisors don’t transact with each other.

What LPL has instead is a scale flywheel: more advisors lower the per-advisor cost of running the platform, which funds better economics, which attracts more advisors. The loop has the same self-reinforcing shape as a network effect, but a different engine driving it: cost economics, not cross-user value.

That’s why LPL’s strongest competitive factor is its switching costs plus cost advantages, not network effects.

Putting It Together

Scale produces the cost advantage; the cost advantage funds the payouts and services that build switching costs; switching costs lock in the assets that sustain the scale.

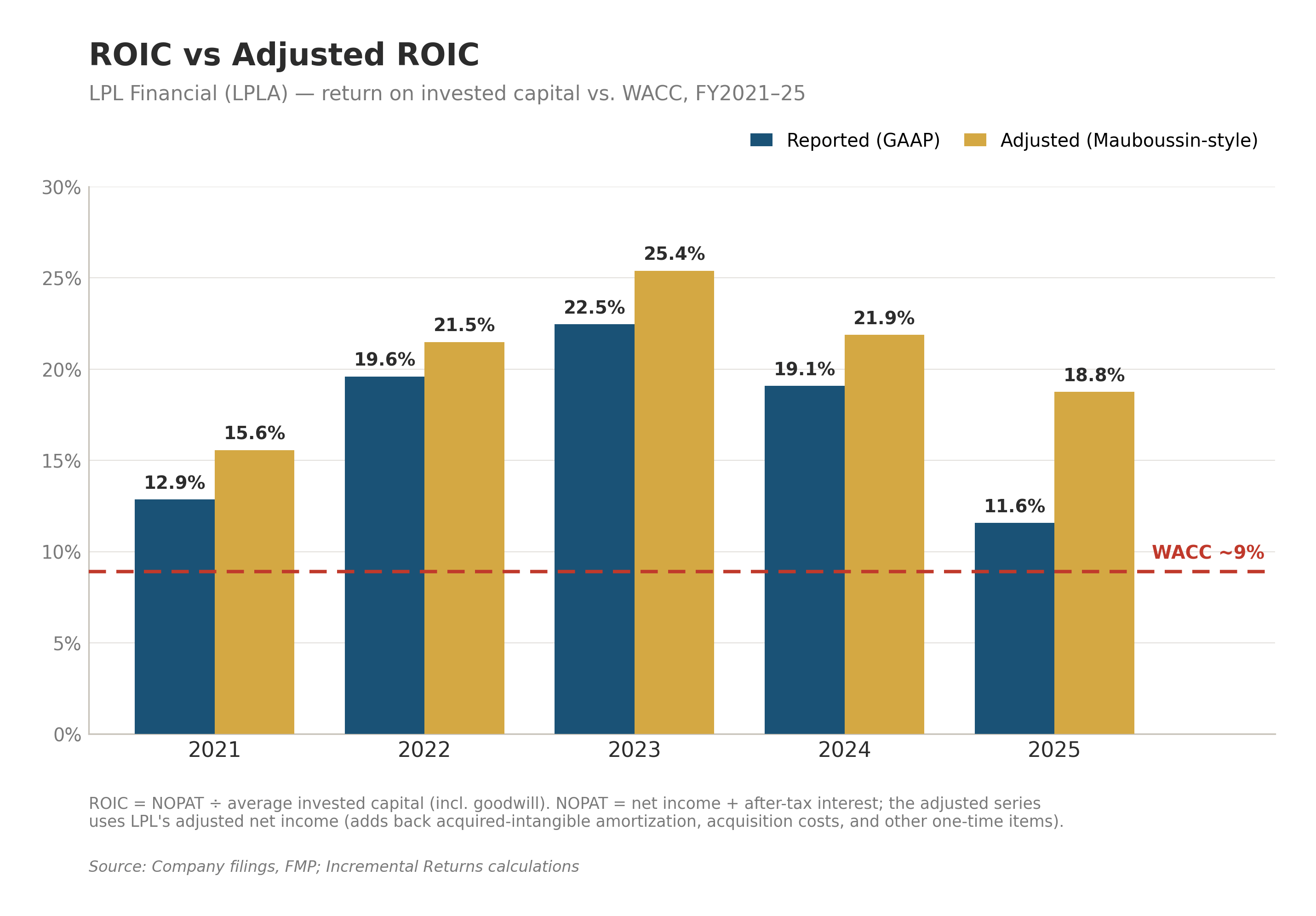

This flywheel is why LPL’s adjusted ROIC has averaged around 20% over the last five years and consistently exceeds its cost of capital.

Also, the independent advisor industry is fragmented and consolidating. Being the lowest-cost platform with scale advantages makes LPL an attractive home for advisors—and an acquirer of other competitors (LPL just bought Commonwealth for $2.7B)—to plug into its flywheel. That gives the company a long runway of growth and reinvestment to strengthen and widen its “moat.”