Invert, Always Invert

The screen that caught Carvana, Wayfair, and Roku before they collapsed and what it's flagging today.

In 1887, the German mathematician Carl Gustav Jacob Jacobi gave a piece of advice that Charlie Munger would repeat throughout his life.

Man muss immer umkehren.

Invert. Always invert.

Jacobi was talking about hard math problems that were resistant to the usual direct assault. But when you flip them around and ask a different question, the problem becomes much easier to solve.

Munger took the same idea and applied it to investing.

Don’t ask how to get rich. Ask how to stay poor, and then avoid that.

Don’t ask which stocks will win. Ask which stocks tend to lose, and start by not owning those.

It’s a powerful reframing.

What to Avoid

In 2008 Cooper, Gulen, and Schill published their paper looking into the asset growth anomaly. What they found was firms that grow their total assets aggressively go on to underperform the market by roughly 8 percentage points a year on a value-weight basis and this is sustained over five years.

The anomaly builds on two other anomalies. Pontiff and Woodgate found that net stock issuance predicts for returns. Then Titman, Wei, and Xie showed the same for abnormal increases in capital expenditures (Capex).

Companies that grow their asset base aggressively are usually doing one of three things: issuing equity at a rich multiple to fund growth they can’t fund internally, acquiring assets at poor prices, or increasing Capex into a trend they think is secular but is, in fact, cyclical (or less robust than they thought).

These companies disappoint because overzealous acquisitions get written down, the incremental returns on increased Capex trend toward the cost of capital (producing little excess value for shareholders), or the high-flying stock price used to fund growth re-rates lower, stunting future growth.

Taking Munger’s advice and inverting the investment puzzle, the companies and stocks we want to avoid are the aggressive overinvestors.

The Screen

I started with every name in the S&P 500 and 400 (midcap) and then filtered for companies with a market cap greater than $5 billion at the rebalance date.

I then applied three filters. First, organic asset growth, total assets ex-acquisitions, in the top quintile. Second, external financing as a percentage of prior-period assets in the top quintile. Third, EV/Sales in the top quintile.

The screen produces ~30 names per year. Each name had to be flagged using only data that would have been known at that moment. The basket was equal-weighted, rebalanced annually at year-end, and held for 12 months.

The backtest included names that subsequently delisted, held at last observed price, zeroed out if they went away entirely.

The look back window was the last nine years, from year-end 2016 through year-end 2025.

What actually happened

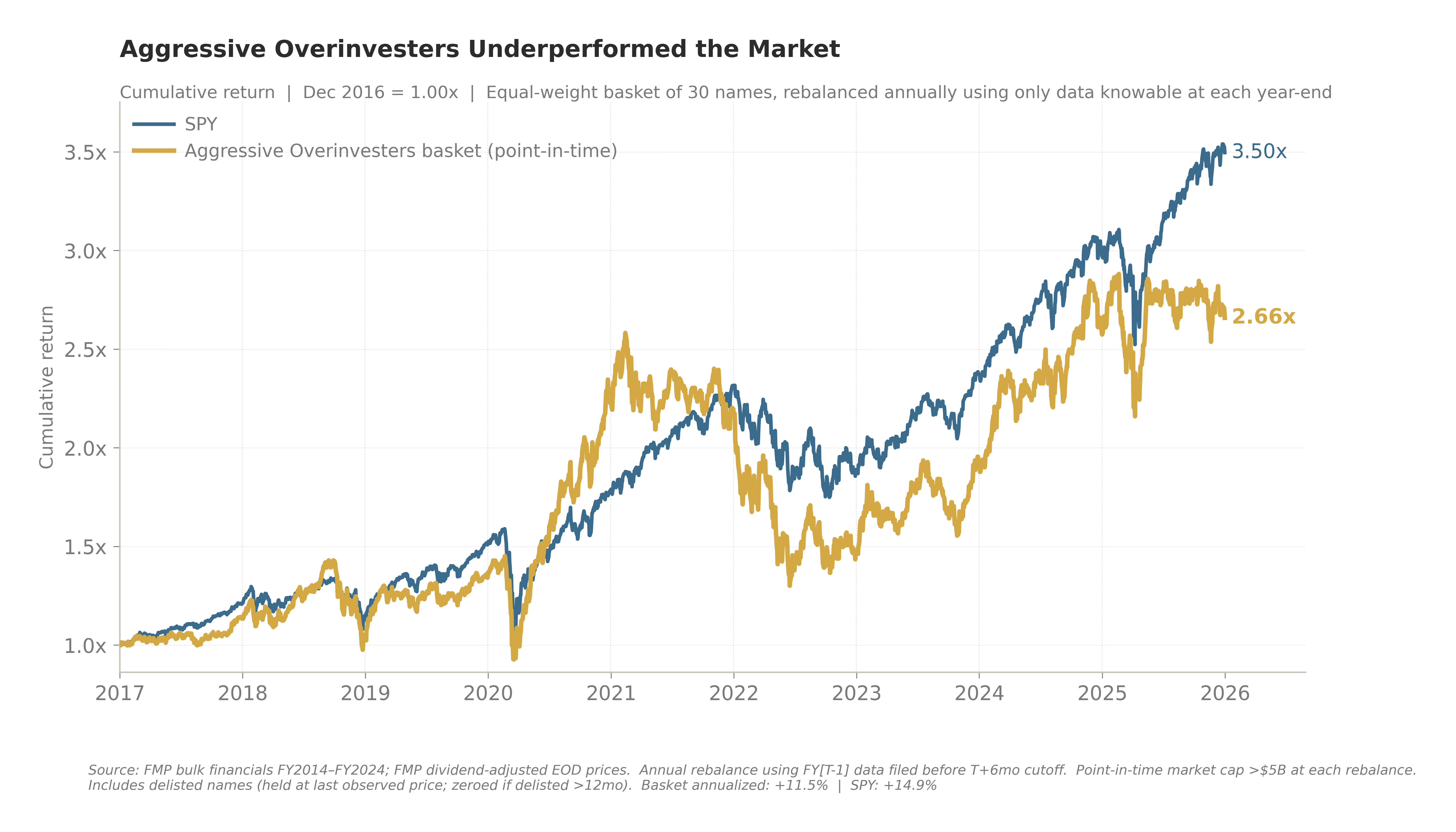

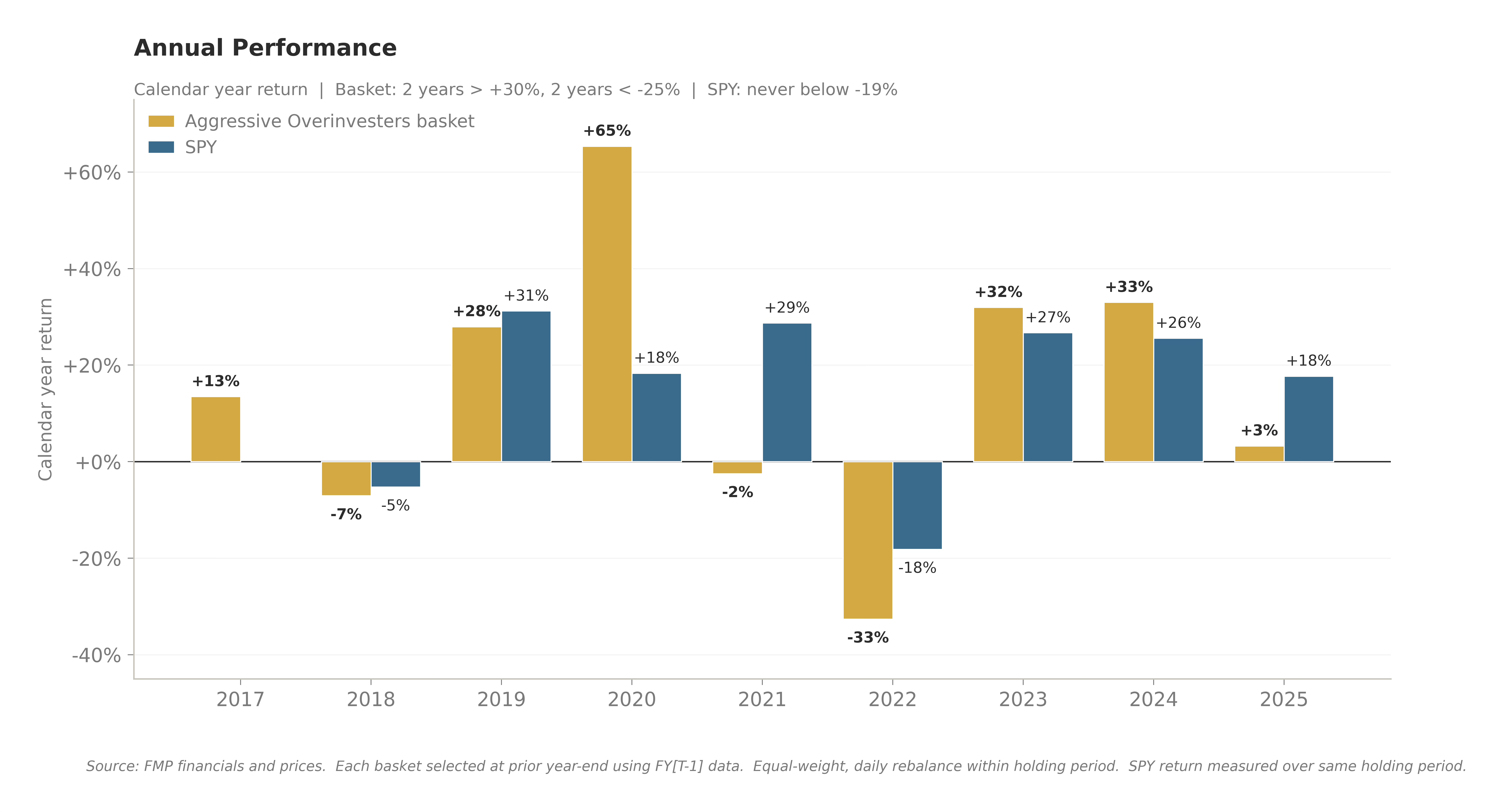

Over the last nine years, the Aggressive Overinvestors basket grew 2.66x vs 3.50x for SPY.

Annualized, that’s 11.5% for the basket against 14.9% for the market. The basket lagged SPY by about 3.4 percentage points a year.

And this is even during an extremely favorable period for aggressive corporate investing with AI infrastructure, GLP-1 buildouts, defense rearmament, and energy expansion.

And there were some strong years for aggressive overinvestors during this period.

The basket put up two enormous years: +65% in 2020, which encompassed the stay-at-home boom with Roku, Wayfair, Carvana, and Chewy leading the way. Then again at the start of the AI infrastructure boom in 2023-2024.

The basket’s worst year was 2022, when it lost 33% against SPY’s 18% drawdown.

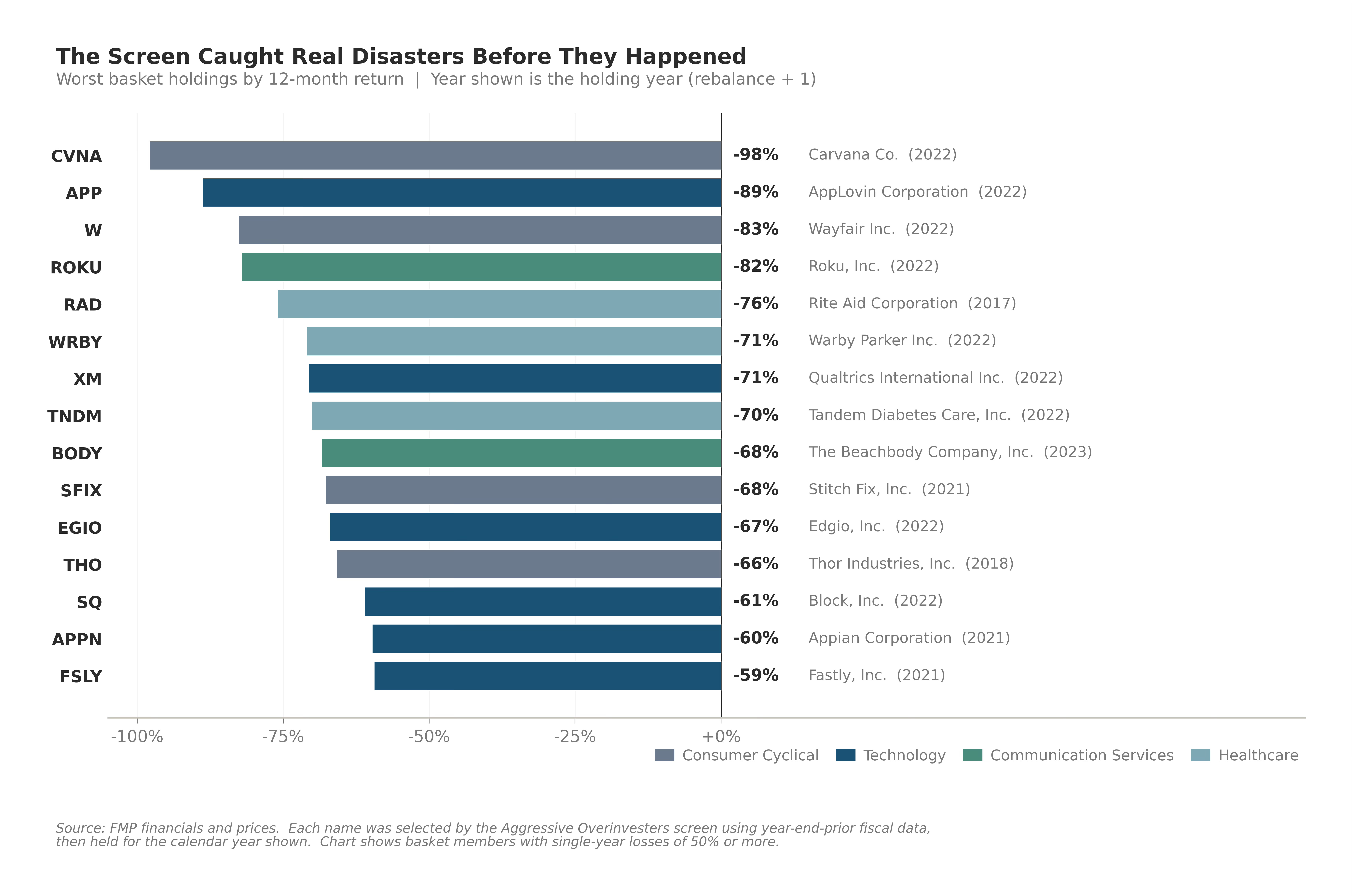

The 2022 basket included Carvana, AppLovin, Wayfair, Roku, Block, Toast, Warby Parker, Qualtrics, Tandem Diabetes, Edgio, and Vicor — twelve names that lost between 48% and 98%.

The Disasters

Carvana, down 98%. AppLovin, down 89%. Wayfair, down 83%. Roku, down 82%. Block, Toast, Warby Parker, Qualtrics — all down between 48% and 80% in a single year. Almost all of them in 2022.

These were among some of the most-discussed, most-recommended, most-owned growth stocks of the prior cycle. They appeared in dozens of newsletter portfolios. They were core holdings of high-flying funds and the narrative for each of them was well articulated

But every single one of them tripped the same set of mechanical filters in the year before they collapsed. Aggressive asset growth, funded by external capital, at a rich revenue multiple.

The screen is not without its drawbacks.

The same screen also flagged Eli Lilly, Broadcom, Palantir, and several other names that performed well through the period. The screen is designed to identify a cohort that underperforms on average. It does not specifically tell you which individual name will collapse.

The goal is to prevent you from owning these dramatic blowups. From permanently impairing your capital.

The goal is to incrementally improve the long-term returns of your portfolio.

But if you’re using this screen for potential shorts, you can’t rely solely on it. It’s a starting point. You will need to dig deeper and create a wider mosaic to try to identify the potential blowups.

Behavioral Checkpoint

I’m not saying this is some binary choice between trying to pick winners or avoiding losers. It’s not a competition because both approaches complement each other.

They can protect you against different mistakes.

Let’s say you think you found your quality compounder. Returns on capital are high, the moat seems real, the management team has a credible plan.

But before you initiate a position you see if it makes the screen for aggressive overinvestors. Is this name in the top quintile of organic asset growth? Is it being funded primarily by external capital? Is it trading at the kind of revenue multiple where the math only works if everything goes right?

If the answer is yes to any of them, you don’t necessarily need to kill the idea. As I said above, it flagged Eli Lilly, Broadcom, and Palantir too. But you need to ask some harder questions and understand why the company is making this screen. Maybe you size the position smaller or have a tighter stop if your thesis is not playing out.

Munger’s advice to invert is essentially a behavioral checkpoint. It asks you to slow down and look at your next great investment a different way because maybe in your excitement about how great this investment is, you overlooked a crucial detail.

Creating a checkpoint slows our thinking down and causes us to engage our more rational thought processes.

Key Lessons

I see three key lessons from Munger’s inversion advice.

The first is that inversion is useful and widely underused. Most investors run elaborate processes to find what to buy with no formal process to identify what to avoid.

The second is that the screen’s real value isn’t as a standalone strategy. Its value resides in being a behavioral checkpoint.

The third is about portfolio management. The point is not to be right about every stock you avoid. It’s about being wrong less often about the stocks you own.

A quality book is a concentrated bet on a small number of companies. The cost of accidentally including a blow-up is enormous. We want to reduce those chances for the long-term health of our portfolio.

What’s in the Basket Today?

The current Aggressive Overinvestors basket is concentrated in three themes: AI infrastructure, GLP-1 manufacturing scale-up, and the post-IRA (Inflation Reduction Act) industrial build-out.

This doesn’t mean all the names in the basket will be losers. Some of them could turn out to be great compounders — especially if their asset growth is in highly productive Capex that generates returns above their cost of capital. But a few of them just might make the list of worst performers.

The full list of names is below for paid subscribers.