The Complete AI Guide to Intuit: Where the Disruption Hits First (and Where Intuit Fights Back)

Credit Karma, Mailchimp, TurboTax, and QuickBooks under the microscope.

Intuit is down almost 50% since initiating a starter position, and then down another 36% after I added to the position and increased its weight to a two-thirds position, based on prior price weakness and my trading rules.

In The Art of Execution, the assassins would have sold out. Given the current market structure and the rise of large pod shops, plenty of assassins are doing exactly that.

I’m not an assassin.

Being the fastest on the button is not my edge, and it is not one I want to cultivate.

I want my edge to be behavioral: the ability to do the hard thing when the market is telling me I’m wrong.

But I also don’t want to be stubborn like the rabbits in the book, doubling down on a losing position that keeps losing because I believe I’m right and the market is always wrong.

Wisdom in crowds exists, but so does madness.

So which is it with Intuit? Is the market right, or is it caught up in short-term AI hysteria?

Either way, Intuit’s recent price action calls for a fundamental review. I want to go through its four major business lines to understand the key AI risks and the counterarguments. Then, using a DCF and a reverse DCF, I want to determine whether current expectations present an opportunity to add to a high-quality business at a discount, or whether the market is right and Intuit is a quality trap?

Credit Karma

Credit Karma is a lead generation machine.

All of its consumer financial services are free. Credit Karma uses your financial information to provide targeted product recommendations. They earn revenue when you accept a recommendation and sign up with a lender.

Credit Karma doesn’t show random ads. Using their proprietary recommendation engine, Lightbox, they pre-qualify each user for each product they recommend. You know before clicking that you’ll likely be approved. That’s why Credit Karma’s recommendations have approval rates above 95%.

There’s an inherent conflict of interest in Credit Karma’s business model. They don’t get paid for giving you the best advice. They get paid when you take action on a product from one of their partners. If Chase pays a higher referral fee than Capital One, Credit Karma has an incentive to show you the Chase card more prominently—even if the Capital One card has better terms for you.

A personal finance AI agent doesn’t have this bias. It could compare every credit card, loan, or insurance product on the market and give you the best one based on your financial circumstances. If the AI agent could also aggregate each bank’s pre-qualification tools, it would cut out the middleman entirely.

Of all the potential AI disruptions, Credit Karma’s recommendation business seems most immediately at risk.

Intuit recognizes this. They’re looking to turn AI into a growth lever.

OpenAI

Intuit just partnered with OpenAI and is embedding their recommendation engine inside ChatGPT.

If you ask ChatGPT “what credit card should I get?”, the answer could be powered by Credit Karma’s Lightbox engine and proprietary data.

Intuit earns the referral fee regardless of which interface you use.

To be fair, this sounds a little like letting the fox guard the henhouse.

One Consumer Platform

Intuit merged Credit Karma, TurboTax, and ProTax into a single consumer business reporting segment.

The idea is these businesses should cross-sell each other and strengthen each other’s value proposition.

TurboTax captures your income and tax data once a year. Credit Karma uses that data year-round to make better financial product recommendations.

Credit Karma’s year-round engagement helps drive existing and new users to the TurboTax platform during tax season.

This self-reinforcing cycle helped contribute to a full point of tax revenue growth in 2025.

Intuit wants to add AI features to Credit Karma like Debt Assistant that helps craft a pay-down plan and Tax Assistant that pre-fills your tax returns based on year-round activity. The more financial tools that are personalized to you, the stickier the platform becomes and the stronger the cross-selling becomes.

Data Moat

Intuit holds roughly 70,000 tax and financial attributes per consumer and generates 60 billion machine learning predictions daily.

A general-purpose AI can give you generic advice about credit cards. Credit Karma’s AI, powered by your actual income, spending habits, credit history, and tax situation, can give you advice that no outside model can match without that same data access.

Credit Karma’s Lightbox technology already drives approval rates above 95% on recommended products. That kind of precision is only possible because of the underlying data. And that data advantage compounds with every new consumer interaction.

Access to your financial data comes down to trust. Credit Karma has already built this trust. Layering AI on top of their current services and your data can help them become a better recommendation platform and help you with your financial health.

The question is: how long until you feel comfortable giving OpenAI or Claude access to your financial data? Given our history of trusting new technology way before we should, I’d say this will happen quickly.

Mailchimp

Intuit’s $12 billion acquisition of Mailchimp was controversial from the start and remains so today. Critics called the purchase price excessive and a clear misallocation of capital.

So why would Intuit pay that much for an email service provider?

The strategic rationale made sense. Mailchimp was the largest ESP with a massive small business customer base. It could serve as a top-of-funnel acquisition channel for Intuit and QuickBooks Online. Many small businesses start collecting customer emails before they need serious accounting software. Mailchimp could capture these businesses early, then cross-sell QuickBooks Online to users who didn’t yet have an email marketing strategy.

Intuit publicly maintains a 15% IRR hurdle rate for acquisitions. Someone at Intuit believed they could clear that bar even at a $12 billion price tag. With the fed funds rate still at 0% when the deal closed, that probably helped the math work.

But that $12 billion price is now haunting Intuit as it raises prices and cuts back its formerly generous free plan while new AI risks emerge.

The AI Threat to ESPs

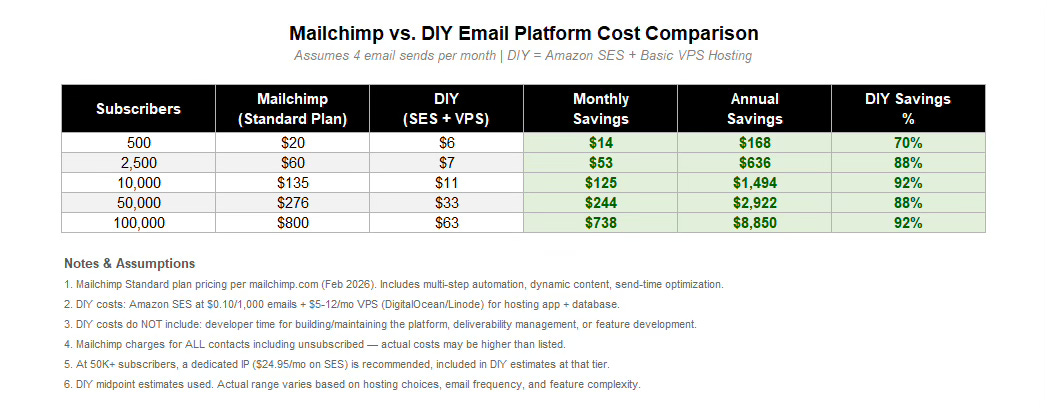

You can’t send mass emails directly from Claude.

But you can use AI tools to generate email campaigns, write copy, design templates, and analyze customer data. And you can vibe code your own ESP, host it on AWS, and use an API call to Amazon SES or Sendgrid to handle email delivery.

You’ll save money doing this.

What this cost breakdown doesn’t factor in is the legal and regulatory hurdles, the ongoing maintenance commitments and costs, and the operational “insurance” a dedicated ESP provides.

Regulatory Compliance

The regulatory hurdles aren’t insurmountable, but they require careful attention.

The two major regulations you need to comply with are CAN-SPAM in the U.S. and GDPR in Europe.

CAN-SPAM violations can cost up to $50,120 per offending email.

GDPR violations could cost up to 4% of your global revenue.

Then there are other anti-spam marketing laws you need to build into your system.

This isn’t impossible. Any competent developer with AI assistance should be able to build a compliant system. It just takes time and attention to detail.

Ongoing Maintenance

Once you’ve built your ESP, you need to maintain it.

You need to handle both soft and hard email bounces, manage complaints from major email providers, and keep your list clean by processing unsubscribes.

The biggest ongoing job is maintaining deliverability. What’s the point of building your own ESP if your emails never reach subscribers? The three main factors affecting deliverability are infrastructure, content, and reputation.

Infrastructure is your email’s ID card. When you send an email, the recipient’s email provider (Gmail, Outlook, etc.) wants to verify you are who you claim to be.

Content is how recipients react to your emails. Do they open them? Reply to them? Click links? Pull your emails out of spam? If email providers see poor engagement with your emails, they’re more likely to automatically route them to spam.

Reputation is how email providers score you based on infrastructure and content. High score means inbox. Low score means spam.

Building a good reputation from scratch takes a long time. Each email provider has its own scoring system. You have to check each one separately and adjust your system based on their feedback. Then you have to adjust again when they update their spam filters or when new privacy regulations take effect. Maintaining deliverability could easily become a full-time job by itself.

For many small businesses, Mailchimp is just their ESP. They built their website on a different platform like WordPress and integrated Mailchimp to collect emails. They’d have to vibe code and maintain these integrations along with any other third-party connections. More integrations mean more ongoing maintenance to ensure everything works and syncs properly.

The big risk with a DIY system: if something goes wrong and you get your domain blacklisted, all this work was for nothing and you have to start over.

The Value Proposition of Mailchimp

Yes, you pay more for Mailchimp. But you’re paying them to save you time, to handle all compliance issues, all maintenance issues, all integrations. And most importantly, you’re paying them to ensure your emails consistently get delivered from a trusted source. You pay for access to their development team so everything works behind the scenes and you simply log in, compose a marketing email, and hit send.

The Real Risk

The risk isn’t every business vibe coding their own ESP to save money. The ESP business is already a commodity. The risk isn’t current Mailchimp subscribers leaving either. The data and operational switching costs are too high.

The biggest risk is that Intuit—trying to justify their $12 billion purchase—raises prices too high too fast and pushes potential future customers to other platforms. This slows customer acquisition and future revenue when these customers eventually need to upgrade their subscriptions. Which is exactly what’s played out in recent quarterly calls.

The Premium Repositioning Strategy

But Intuit could also be repositioning Mailchimp as a premium business-focused ESP. They’re moving Mailchimp away from its roots as an ESP for everyone and positioning it as a business growth tool. They’ve also been pushing harder into mid-market companies who have bigger marketing needs and are willing to pay up for more features.

Layering AI into these services could help Mailchimp retain and grow more business clients. Everything I discussed about what AI can do for email marketing currently has to happen outside Mailchimp. Then you have to go into Mailchimp and implement it manually. If Mailchimp had an AI agent layer, in theory you could have it build your campaign, set up automations, and manage your entire email marketing strategy.

Because small business owners are pressed for time, they’re willing to pay up for features that save them time, reduce operational costs (fewer employees needed), and help increase revenue.

Turbo Tax

The AI Threat to TurboTax

Tax filing is fundamentally a structured data problem. You gather documents, extract numbers, apply rules, and submit forms. Claude has demonstrated it can read PDFs, extract structured data, organize it, and perform multi-step workflows. A capable AI agent connected to your bank accounts and W-2 documents could prepare a return without any software. This threatens TurboTax’s value proposition to the basic DIY market—historically its volume driver.

50% of US tax filers still pay someone $200-500+ to prepare their taxes. Each year TurboTax tries to grab market share in this lucrative “assisted” segment. TurboTax Live has helped them move upmarket because many assisted filers just have one or two concerns they want professional help with. TurboTax Live provides that help for a fraction of the cost of full-service preparation.

But now AI is a competitor in this space too. Potential growth into this lucrative market is either greatly reduced or gone altogether.

TurboTax is Intuit’s second largest business with about $4.4 billion in revenue. Market share loss in the DIY segment plus slower gains in the assisted market would significantly impact Intuit’s current and future value.

Why TurboTax Retains Its Value

Preparing taxes is stressful and time-consuming depending on your financial situation. You want them done quickly and painlessly. Most people will pay for this. That’s why TurboTax is so successful and why the assisted tax prep market is so large.

TurboTax has built switching costs into a product that shouldn’t really have any. They do this by increasing the speed of tax completion without sacrificing quality or accuracy. A key part is TurboTax’s ability to import last year’s returns and pre-fill your basic information.

Current TurboTax customers who are used to the interface, speed, and efficiency are unlikely to build their own process in an LLM. Why would they want to spend more time on taxes? And how would they know it’s accurate?

TurboTax has a team ensuring its systems comply with current federal and state tax codes and work properly. How do you know the LLM’s training is up to date on recent tax law changes? LLMs also hallucinate and make things up when given noisy data. How can a filer trust AI not to make a costly mistake?

TurboTax’s Guarantees and Support

Intuit backs TurboTax accuracy with real money.

It offers an Accurate Calculations Guarantee that pays any IRS penalties from calculation errors. ChatGPT and Claude can’t do that, nor would they want the liability exposure.

TurboTax also provides Audit Defense. If you get audited, TurboTax provides enrolled agents who know the tax code to represent you before the IRS. If you use an AI chatbot, you’re on your own.

How AI Can Enhance TurboTax

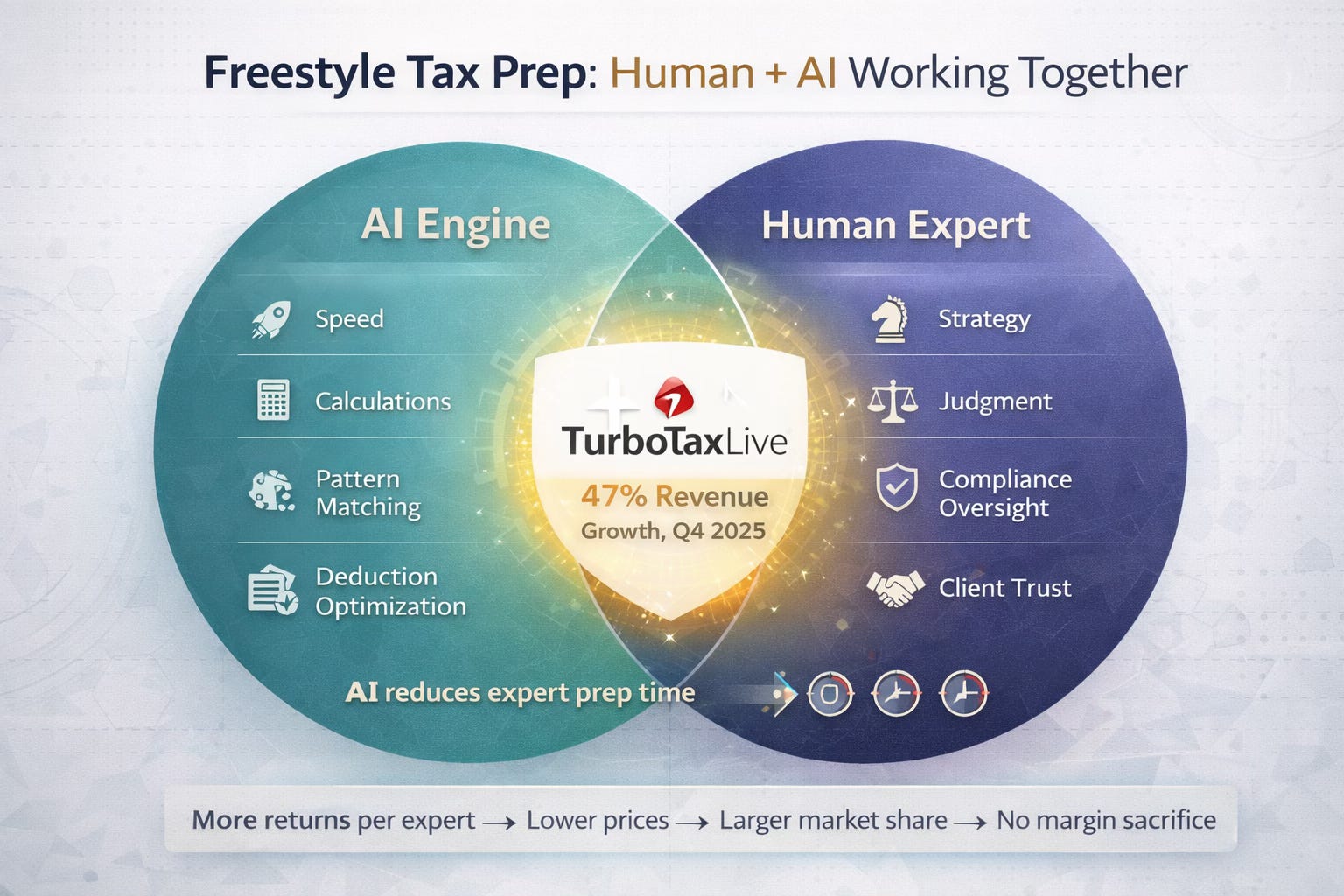

AI implementation can also help TurboTax increase its speed, accuracy, and personalization. It could include real-time accuracy checks, enhanced prompts for better deductions and credits based on what similar taxpayers have claimed, and an assistant to answer each filer’s specific questions.

TurboTax Live has been successful. As of Q4 2025, TurboTax Live grew 47%—well ahead of management’s 15-20% revenue growth expectations. AI should have the largest positive impact on TurboTax Live.

It’s hard to scale one-on-one professional help, which is why TurboTax has made only small inroads into the assisted tax prep market. But AI tools can reduce the time experts spend preparing a return by about 20%. Every hour saved per return means more returns per expert, which means Intuit can serve more of the assisted market without proportionally growing headcount.

This also allows Intuit to lower TurboTax Live’s price without sacrificing margins, expanding market share and profits.

The example I keep referencing with AI is freestyle chess—human and computer working together. The computer does the calculations and the human oversees the strategy.

Intuit offers Expert Full Service for far less than traditional assisted tax preparation. Using AI to scale this service can help TurboTax gain more assisted market share, increasing revenue.

The E-Filing Advantage

Finally, no LLM is an authorized e-filer. You still have to print your taxes and mail them in. TurboTax is an IRS-registered e-filer.

Will LLMs eventually try to register as e-filers? Maybe, if the rules change. Right now only a real person can apply. But if they do, they’re taking on increased compliance costs, data security costs, anti-fraud costs, and overall liability. Do they want that, or would they prefer to sell their LLM to a company that can layer it on top of existing compliance infrastructure?

QuickBooks Online (QBO)

QuickBooks is Intuit’s biggest revenue source, generating about $12 billion.

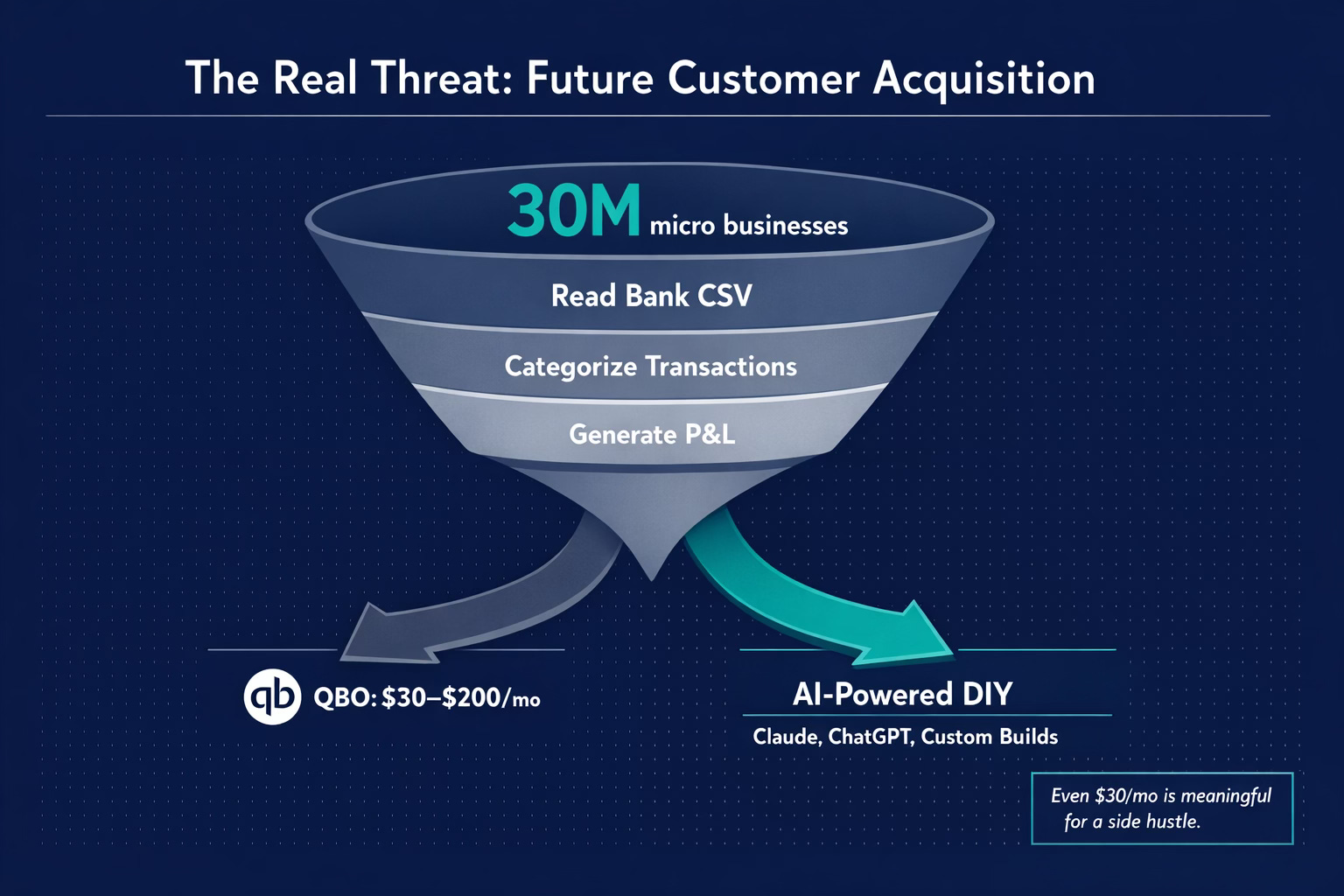

Like TurboTax, QuickBooks is built around the basics: categorizing transactions, reconciling bank feeds, generating profit-and-loss statements, creating invoices, and tracking expenses. These are exactly the kinds of structured data workflows LLMs and AI agents are good at.

The concern is not that QBO gets replaced overnight. Switching costs are too high for a small business already running on QBO to risk an unproven, vibe-coded DIY system just to save $30–$200 a month.

The Real Threat: Future Customer Acquisition

If you’re a solopreneur starting a landscaping business, do you really need a $30–$200 monthly subscription just to categorize fuel purchases and truck payments?

Claude or ChatGPT can read a bank CSV, categorize each transaction, and generate a clean P&L in minutes. You can even build a dynamic financial statement in Excel with Claude’s extension.

So Intuit either fails to win these new customers and loses future growth, or it has to spend more to win them, which compresses margins.

There are an estimated 30 million micro businesses in the U.S., including solopreneurs, freelancers, gig workers, and side hustles. Even $30 a month for QBO Simple can be a meaningful expense.

QuickBooks is utilitarian. It meets most needs for most businesses, but it will not meet every need for every customer. Technically savvy business owners could build custom financial management tools. Or a developer could build a consulting business that helps small businesses spin up an accounting system that pulls bank data via Plaid, uses AI to categorize transactions, and generates reports tailored to specific needs.

That is not most business owners today, but the population capable of doing this will grow as the tools get easier to use.

The Accountant Channel: Strength and Vulnerability

QBO’s most powerful distribution channel is the accountant channel.

Approximately 600,000 accountants in the U.S. are trained on QuickBooks and recommend it to clients. Businesses use QBO because their accountant prefers it, and accountants prefer QBO because most clients use it.

But the Illinois CPA Society believes bookkeeping is likely to be one of the most disrupted functions due to AI in the coming years. Again, double-entry accounting is a set of rules applied to structured data.

Fewer accountants means fewer QBO recommendations to small business owners. Without a nudge from an accountant, a small business might choose a QBO competitor or handle it themselves with AI’s assistance. Then QBO’s two-sided network, one of its strongest competitive advantages, begins to unravel.

Domain-Specific Intelligence: QBO’s Structural Edge

QBO has domain-specific intelligence. The platform is trained on hundreds of millions of small business financial transactions across every industry and vertical. AI trained on this data will enhance its value proposition.

For example, a general contractor pays United Rentals $4,500. A general AI sees an equipment company and categorizes it as an equipment expense, but the treatment depends on the job. A backhoe for a specific client job is a direct job cost and should be labeled as such to properly analyze job profitability. But a generator for the contractor’s office trailer is an overhead expense. Same vendor, same transaction type, different accounting treatment.

Or consider an e-commerce brand that receives a deposit from Shopify Payments for $12,450. A general AI may log it as revenue. But that $12,450 is gross sales minus Shopify’s processing fees. It may also include sales tax collected that is not revenue at all. It is a liability owed to state tax authorities. Correctly entering the deposit requires decomposing it into gross revenue, processing fees (an expense), and sales tax payable (a liability). QBO integrates with Shopify and is trained on millions of these transactions. It knows to automatically unbundle the deposit and route each component to the correct account.

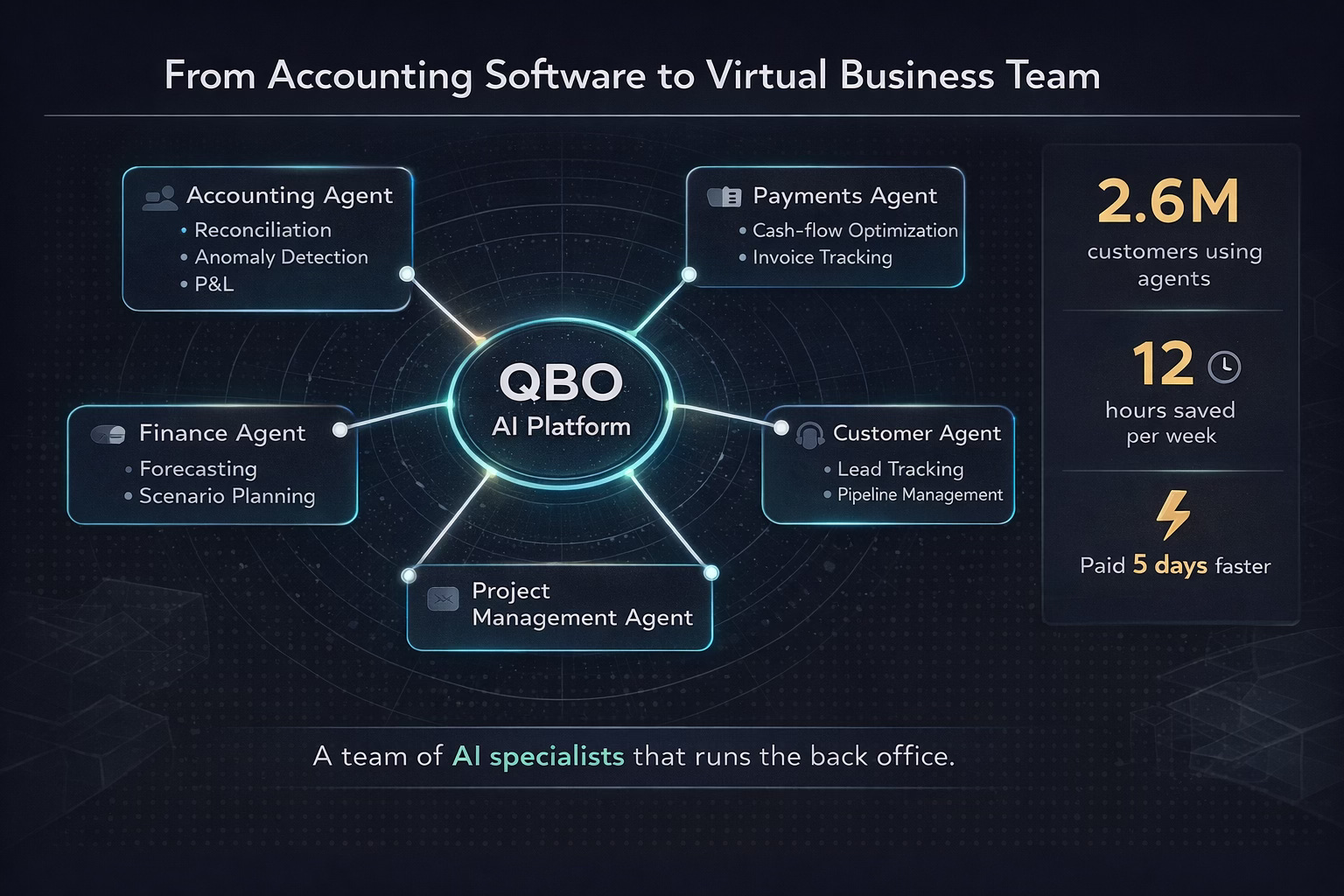

From Accounting Software to Virtual Business Team

With its vast trove of data, QBO with an AI agent can transform from accounting software into a virtual business team.

The agent spans multiple functions: Accounting Agent (reconciliation, anomaly detection, P&L generation), Payments Agent (cash-flow optimization, invoice tracking), Finance Agent (forecasting, scenario planning), Customer Agent (lead tracking, pipeline management), and Project Management. It operates autonomously and executes multi-step workflows without intervention.

The 2.6 million customers already using these agents have reported saving 12 hours per week and getting paid five days faster. A shorter cash conversion cycle can make a business more agile and give the owner more room to invest quickly and take advantage of growth opportunities before competitors.

QBO’s pitch shifts from accounting software to a team of AI specialists that runs and streamlines the back office, so owners can spend more time on the work that grows the business.

Moving Upstream: The Mid-Market Opportunity

Layering AI agents onto the platform should also help Intuit move upstream into mid-market businesses. Mid-market customers need more complex solutions and come with a higher compliance burden. But they also have higher switching costs, higher revenue, and longer lifetime value.

Intuit estimates there are 1.7 million such businesses, defined as those with revenue between $2 million and $100 million. 800,000 already use QuickBooks.

By using AI to customize Intuit Enterprise Suite for specific verticals, Intuit hopes to capture more share within the mid-market. It recently launched an ERP specifically for construction, a $2 trillion industry.

And rather than weakening accountant distribution, AI could strengthen it. QuickBooks with AI can make accountants more productive and allow them to handle 2–3x more clients. Accountants are unlikely to shift away from the platform that drives their business and increases profitability. They would lean further into promoting it, which increases the number of small businesses using QBO.

Finally, Intuit’s development teams will use AI to increase productivity and ship features faster. QuickBooks will not stand still. It will improve faster and become easier to customize for each business’s needs, strengthening its value proposition and cementing its role as a central nervous system for small and mid-market businesses.

Please upgrade your subscription to paid if you would like to see my updated valuation assessment and portfolio action plan.