Does Anthropic Have an Economic Moat?

Switching costs, barriers to entry, network effects run against a $965 billion valuation.

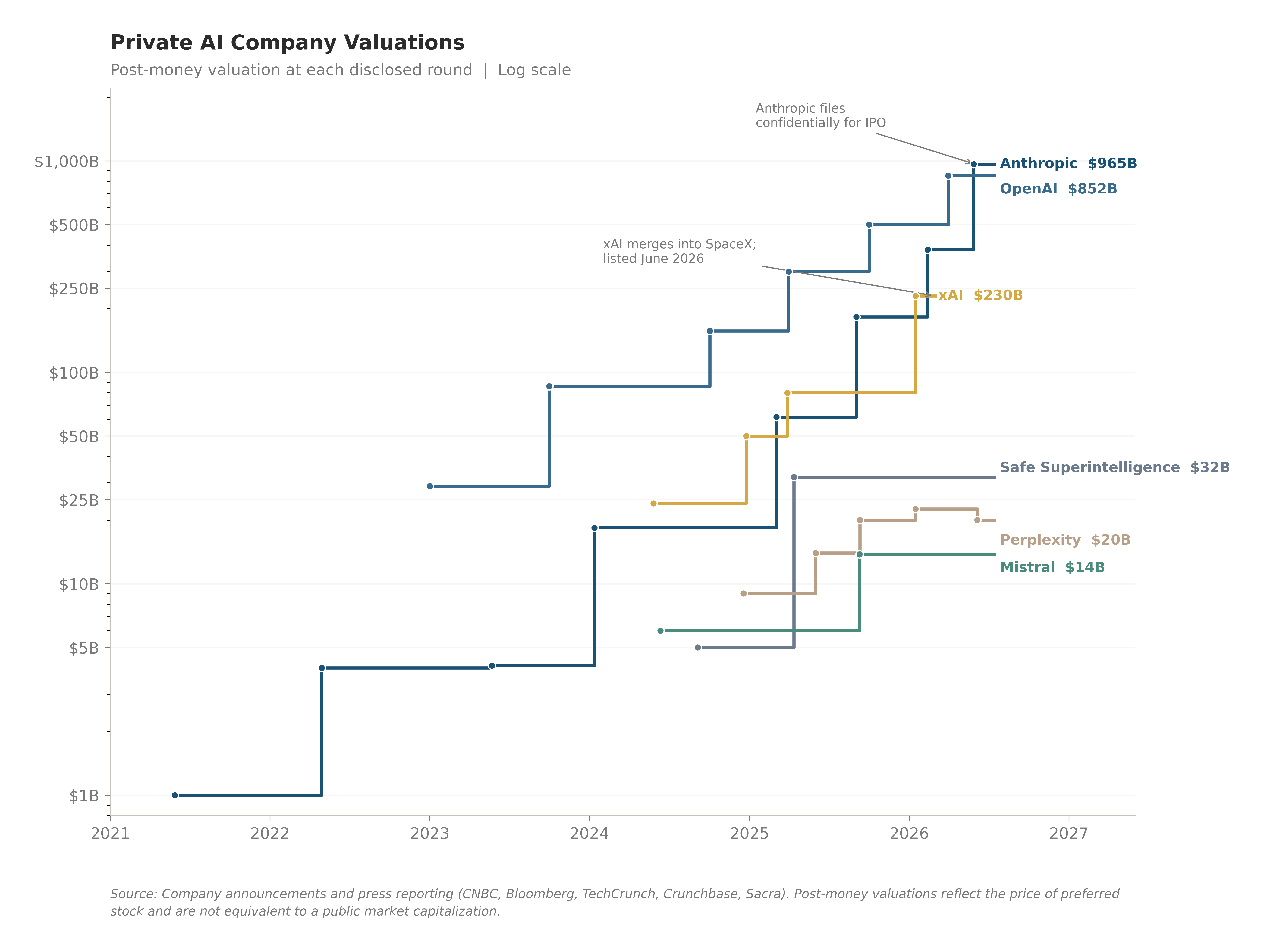

On May 28, Anthropic closed a $65 billion round at a $965 billion post-money valuation, overtaking OpenAI’s $852 billion. Four days later, it filed confidentially for an IPO. Bankers expect a listing sometime between late 2026 and the first half of 2027.

At that valuation, it’s worth asking, does Anthropic have an economic moat?

Below, I run through switching costs, barriers to entry, scale advantages, and potential network effects to see whether there’s an economic moat, or at least the beginnings of one, that could justify a likely $1+ trillion public debut.

Rented vs. Owned

As I evaluate Anthropic’s emerging competitive advantages, I keep coming back to a simple question: what is rented, and what is owned?

Anthropic’s compute is rented (Nvidia, Amazon, Google).

Its talent is rented, and the lease is short. Every day, employees get lucrative offers to leave.

Its capital is rented. None of the leading LLMs are self-funding; they run on investors who eventually want their money back, plus a return.

Its distribution runs through Bedrock and Vertex, rented from two companies that also ship rival models.

Almost every advantage on the list is leased.

That’s not a criticism. Many companies start with rented advantages. Boston Beer Co. (Sam Adams) rented brewing capacity (contract brewing) before it had the capital to own a brewery.

The question is whether the rented advantages convert into owned advantages before the lease runs out?

Switching costs

A while back, I wrote a post about the different switching costs and ranked them by strength. Here, I’ll run Anthropic through the same framework.

From weakest to strongest:

Financial

Time-based

Relationship

Technical/operational

Ecosystem-based

Financial costs

Financial switching costs are largely absent. It’s twenty dollars a month, no termination fee, no equipment. Competitors can discount aggressively or offer incentives to pull users away. This is the weakest rung, and for Anthropic, it barely exists.

Time-Based Costs

Time-based costs exist, but they range from minimal to annoying. A lot ports over: skills, memory, files. What doesn’t port cleanly is fine-tuning and the tacit craft that emerges after many iterations. The core transfers; the finer details often land close enough that you don’t notice what broke until you’re mid-workflow and the output is subtly wrong.

Then you’re stuck reviewing dozens of skills to find the failures. The initial hurdle can feel small, but the costs can spike after you’ve already switched. At that point, you face a sunk-cost choice: finish the changeover and re-tune, or retreat to the model you left.

Relationship Costs

Relationship costs don’t exist unless you’re one of the people who has succumbed to AI psychosis and fallen in love with a chatbot.

Technical/Operational Costs

The Inverted Learning Curve

The main technical hurdle is the learning-curve trap. The old saying applies: you can’t teach an old dog new tricks. Once you have mastered a piece of software (or your organization has), switching can be prohibitive because you have to relearn workflows and absorb a productivity shock.

LLMs invert this problem.

They are easy to start using. You can text or talk to them directly. You don’t need a training course to ask a question, and the product teaches you as you go. Not sure how to create a skill? Ask it. Not sure what the next step in a workflow is? Ask it.

There is still a learning curve in getting better at prompting, but it’s manageable. Once you master prompting in one LLM, much of that skill transfers to others.

The Enterprise Break

Everything changes once the user count goes above one.

A single person re-tuning a dozen skills is an annoying weekend. An organization revalidating four hundred skills is a project nobody wants. By then, the model often stops being a tool that a single employee is responsible for. It runs unattended, checking code before it ships and interfacing with internal systems through a web of connectors.

As the shared corporate context accumulates inside the model, it becomes harder to transfer. This is the classic data trap.

Ecosystem

The highest ranking switching cost is the ecosystem, and this is what Anthropic is targeting

Let’s look at what shipped last quarter.

Cowork launched in February. It sits on your desktop and can run all sorts of daily tasks for you unsupervised. Claude embedded itself inside Excel, PowerPoint, Word, Outlook, Slack, Gmail, and Google Drive. Everything you need to get your work done and to increase your productivity. Now Claude can follow one conversation across an email, a spreadsheet, and a deck without being re-briefed at every transition.

This shared context is their efforts to build an ecosystem.

For example, an analyst pulls comparables from an open workbook, builds the comps table in Excel, drops the valuation summary into the pitch deck, and drafts the note to their MD. The dataset gets explained once. Every application Claude touches makes the next one more useful, because the context carries across the workflow.

Then there’s the marketplace.

Anthropic gave enterprise administrators private plugin marketplaces. These are internal app stores, sourced from a company’s own code repositories, with admin control over what employees can install.

Anthropic shipped prebuilt plugin templates for HR, engineering, operations, financial analysis, investment banking, equity research, private equity, and wealth management. And it put Skills into the Excel and PowerPoint sidebars, so a firm can save its proprietary analysis or its approved slide template as a one-click action for every employee.

It’s like skills but scaled up to a firm-wide level, with an admin console bolted on. Employees don’t own the skill and can’t move it to their preferred LLM. They have to stay within the firm’s ecosystem built on Anthropic.

The Landlord Problem

But there is one problem with the strategy right now.

Claude in Excel is an Office add-in. Excel belongs to Microsoft. Microsoft is an investor in Anthropic and wants its investment to do well. But Microsoft also has Copilot, which competes directly with Claude.

The ecosystem is being built on apps it doesn’t own. The landlord is friendly, for now.

The plugin architecture is similar.

It’s API-based and broadly compatible with the specification everyone else already uses, so integrations built for other systems port over without much work. That fills a marketplace fast.

But it’s the MCP issue all over again.

The one piece Anthropic owns is the shared context layer. The thing that holds your workbook, your deck, and your thread in mind simultaneously. This is proprietary, and nobody else has shipped a competitor.

Yet.

Almost everything else I’ve described above is scaffolding. Skills, memory, connectors, plugins. It sits on top of the model, and it is the thinnest layer in the entire stack.

It is also exactly what a competitor’s migration tool would target first.

Network Effects

Similar to switching costs, I also ranked six types of network effects, from weakest to strongest.

Direct Network Effects

My initial thought was that Anthropic might benefit from direct network effects: more users create more training data, which improves the model, which creates more value for every new user.

But I think that’s wrong.

Frontier capability comes from compute, reinforcement learning, and synthetic data, not from increased user activity. The counterexample is DeepSeek. Its users and traffic are a rounding error relative to Anthropic’s, yet it still achieved meaningful capability. The same is true of Mistral and Qwen.

Anthropic can train on consumer conversations by default. But its commercial products (Claude for Work, the API, Bedrock, Vertex) are contractually excluded from training. The data Anthropic can learn from is mostly retail consumer chatter, which is comparatively low value.

The data that might actually create compounding effects, enterprise workflows and context, is walled off by the privacy guarantees that help Anthropic win those deals.

Data Network

At best, this looks like a data network, which ranks near the bottom. It’s also vulnerable: competitors with better technology can win quickly, and in AI, that happens often.

There isn’t a true direct network effect here. There is a narrower effect where usage generates failure telemetry and evaluation sets. That can improve the product, but it doesn’t reliably improve core capability, and it doesn’t compound the way search queries once improved Google’s index.

Indirect Network Effects

An indirect network effect occurs when more usage of a product attracts more valuable complements, which then make the original product more valuable.

The classic example is Intuit’s QuickBooks Online. With a large installed base, it becomes worth ADP’s time to build payroll integrations, and PayPal’s and Square’s to build payments. Those complements make QBO more useful, which attracts more users, which attracts more complements.

AppFolio ran the same play. Open the API, let third-party tools integrate, and each new connection makes the platform harder to rip out.

The LLM version looks similar. Notion, Canva, Gmail, PitchBook, Slack, Stripe, and thousands of other vendors have shipped MCP servers that plug their software directly into models.

SDK downloads reportedly went from roughly 100,000 in the first month after launch to 97 million a month by March 2026. The complements are arriving exactly as the framework predicts.

But there’s a problem.

ADP built to QuickBooks’ API. That integration works with QuickBooks and nothing else.

MCP is not exclusive.

Anthropic published it in November 2024. OpenAI adopted it in March 2025, Google in April, and Microsoft announced support at Build. In December 2025, Anthropic donated the protocol to the Linux Foundation’s Agentic AI Foundation (backed by AWS, Google, Microsoft, OpenAI, Bloomberg, and Cloudflare).

So when a software company like Notion ships an MCP server, it works with Claude, ChatGPT, and Gemini at close to zero incremental cost to Notion.

Anthropic built the foundation for indirect network effects, then gave away the exclusivity that would have allowed those effects to accrue primarily to Anthropic.

I understand why.

In 2024, no one had enough market share to force a proprietary standard. An open protocol that everyone adopts beats a closed standard that no one uses. MCP helped induce demand for the whole industry.

The top three network effects(social, multi-party, two-sided marketplace) don’t apply here.

Anthropic’s best shot at network effects was a protocol network. But as discussed, it donated that advantage to accelerate broad adoption.

Barriers to Entry

The barrier everyone thinks of first is capital.

Leading AI labs are burning cash, and there is a finite pool of capital. Why wouldn’t the largest, most likely winners absorb the money and starve everyone else?

But capital is still flowing. Frontier Labs hasn’t had trouble raising. Neither has Mistral. Even xAI was able to raise before its merger with SpaceX.

The real barriers are less headline-friendly.

Compute Allocation

The constraint isn’t simply that a startup can’t afford chips. Supply is so tight that many teams can’t get chips at any price. Allocation is relationship-mediated, and it flows to counterparties with long-term commitments and a high likelihood of existing in five years. Suppliers ration to likely survivors. That becomes a self-reinforcing cycle.

Talent Concentration

The number of people who have personally run a frontier-scale training program is measured in the low thousands globally. Compensation to secure that talent is soaring. Meta reportedly paid one person $250 million.

Trust and Compliance

SOC 2, HIPAA, FedRAMP, indemnification, and model-behavior guarantees are boring, but hard to replicate quickly. Reputation for safety is built one company at a time.

Distribution

Bedrock and Vertex are the enterprise front door.

A counterargument is that these barriers mostly protect the frontier. That matters only if the bulk of value stays at the frontier. If “good enough” keeps getting cheaper, the key question is whether marginal customers will keep paying for frontier capability.

Scale Advantages

Scale today means a training run amortized over far more inference, better unit economics per token, and inference optimization that smaller competitors can’t match.

Tight compute supply also advantages the largest players. Suppliers prioritize the labs with the best odds of long-term survival and the most reliable revenue, reinforcing the cycle described above.

But again, Anthropic owns no fabs, chips, or data centers. It rents all of it from companies that also fund competitors and, in the case of Google and Amazon, sell rival models to the same customers.

Anthropic may have real scale advantages, but they sit on leased real estate.

Token costs are also falling, so it’s worth asking how durable that cost advantage is over time.

The Moat

My initial gut reaction was that Anthropic might develop an emerging moat built on high barriers to entry (mostly capital constraints), scale, and potentially both direct and indirect network effects.

After walking through the factors, what I’m left with is narrower: an emerging moat built primarily on switching costs in the B2B enterprise market, supported by scale and barriers to entry, but not the capital constraints I assumed would matter most.

We’ll learn more when the S-1 drops and regular financial disclosures begin.